A Fed head says watch the data

and the market looks the other way

Yesterday my favorite Fed Governor, Chris Waller (Go Cougs!), spoke at the Rocky Mountain Summit Global Independence Center in Victor, Idaho. He spoke at length about the dual mandate, the tight labor market, and the persistently high inflation. Then he laid out what he believes is the “path of monetary policy”. He stated that,

“…with inflation so high, there is a virtue in front-loading tightening so that policy moves as soon as is practical to a setting that restricts demand.”

The idea of restricting demand has been a constant theme from the Fed since they acknowledged that the inflation was no longer transitory. This is MMT playbook stuff. Keep this idea of demand restriction in mind. It’ll come into play in just a moment. He then goes on to explain in detail what the Fed’s FOMC meeting is going to look like.

“…it should not be surprising that looking toward the FOMC's next meeting July 26-27, and with the CPI data in hand, I support another 75-basis point increase, bringing the target range for the federal funds rate to 2-1/4 to 2-1/2 percent before August.”

A 75 point increase is now baked into the cake. However, he leaves the door open for something more.

“However, my base case for July depends on incoming data. We have important data releases on retail sales and housing coming in before the July meeting. If that data come in materially stronger than expected it would make me lean towards a larger hike at the July meeting to the extent it shows demand is not slowing down fast enough to get inflation down.”

There it is. That was suppose to be the market’s signal. If RETAIL SALES and HOUSING DATA come in “MATERIALLY STRONGER”, “expect.. a larger hike”.

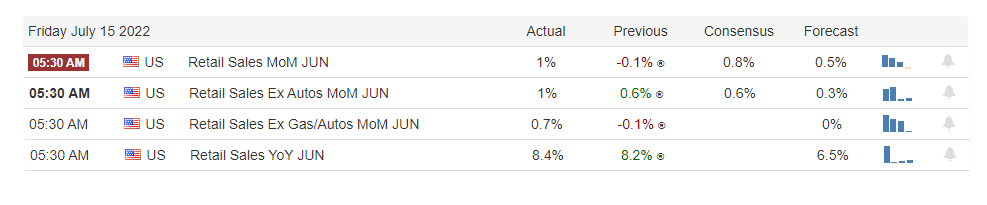

Today retail sales data came out and it surprised to the upside across the board.

This should have been the signal to the market that a 100 basis point increase in the Fed Funds Rate was now “on the table”. Instead, the market decided to chase the squirrel at the University of Michigan’s “Expected Change in Prices” consumer survey which showed a moderating of inflation expectations.

March and April expectations came in at 5.4%. May and June, 5.3%. Now July’s preliminary number is 5.2%. This caused the market to take off. The thinking goes, if inflation expectations come back in line, the Fed can stop fighting actual inflation.

Circling back to Waller.

“I judge that level (2.25-2.5%) is close to neutral, by which I mean a level that neither stimulates nor restricts demand, assuming that the economy is growing moderately (at its potential) and unemployment is roughly where it is now.”

Recall that we’ve had Fed heads say that we need to get the rate above neutral. Waller himself stated that he wanted to set monetary policy to a level that “restricts demand”. He reiterates this fact later in his speech.

“Based on what we know about inflation today, I expect that further increases in the target range will be needed to make monetary policy restrictive, but that will depend on economic data in the coming weeks and months.”

That data that he is going to be reviewing between the July and September meetings will be employment and CPI data. He wants to see inflation moving down before he lets off the brakes.

“I think we need to move swiftly and decisively to get inflation falling in a sustained way, and then consider what further tightening will be needed to achieve our dual mandate.”

The Fed is looking in the rearview mirror attempting to drive the economy forward. They have blown one of the biggest bubbles in economic history. In an attempt to reduce it, they opened up the reverse-repo spigot. Now they are draining liquidity in the overseas markets. This does not purport to end well. Next week we’ll get some housing data and margin debt statistics. This last month has enjoyed positive (although choppy) gains in the market but unless the money supply and margin debt statistics show otherwise, these rallies will be short-lived.