An explosion rocks Wall Street

all traders are on edge for tomorrow

US Producer Prices have rocketed higher. The year-over-year increase for Final Demand: Finished Goods came in at 13.6%!

Even the so-called ‘core’ of finished goods less food and energy is running 5.9% year-over-year higher.

These are blow-out numbers. Wall Street forecasts were not close on this one. It caught many by surprise.

Soon, these high numbers that producers are paying for goods will trickle down to the consumer level. This has put traders on high alert. Everyone is quickly becoming aware that the Fed is in trouble here. They have to increase the taper which will reduce market liquidity. The market is now coming to terms with the fact that reducing the loose monetary policy of the Fed is going to be restrictive of market growth. If you don't understand liquidity or what a lack of it means, I highly recommend this letter to investors from Howard Marks.

Mr. Marks is the co-founder and co-chairman of Oaktree Capital Management, a firm with a net worth north of $2 billion. He has been in this game for a long time. He started at Citigroup in 1969 and started Oaktree in 1995. His letter to investors was written in March of 2015 but it has timeless qualities that are very pertinent to today.

All eyes are now on the Fed. The market hangs in the balance with their announcement tomorrow. I expect Fed Chairman Powell will try to walk the tight rope of acknowledging that inflation has gone hot and the need to reassure investors that the Fed is in control. He will most likely announce an increase to the tapering plans of the Fed. Large Wall Street banks are all on record thinking he will double the pace. The Fed’s previous announcement of the taper stated that it was reducing Treasury purchases by $10 billion and mortgage-backed securities by $5 billion. If both are doubled, the Fed will be purchasing $20 billion less in Treasuries and $10 billion less in MBS. This is a lot of liquidity to be removing from the market.

The central bank’s previous attempts to taper their asset purchases has never panned out. This is because tapering is tightening. The Fed has fueled bubbles with their excessive liquidity and by reducing that liquidity, it would tighten the market. They’ve also succumbed to believing the stock market is the economy and that any little wobble in the stock market needs their attention. This means more liquidity.

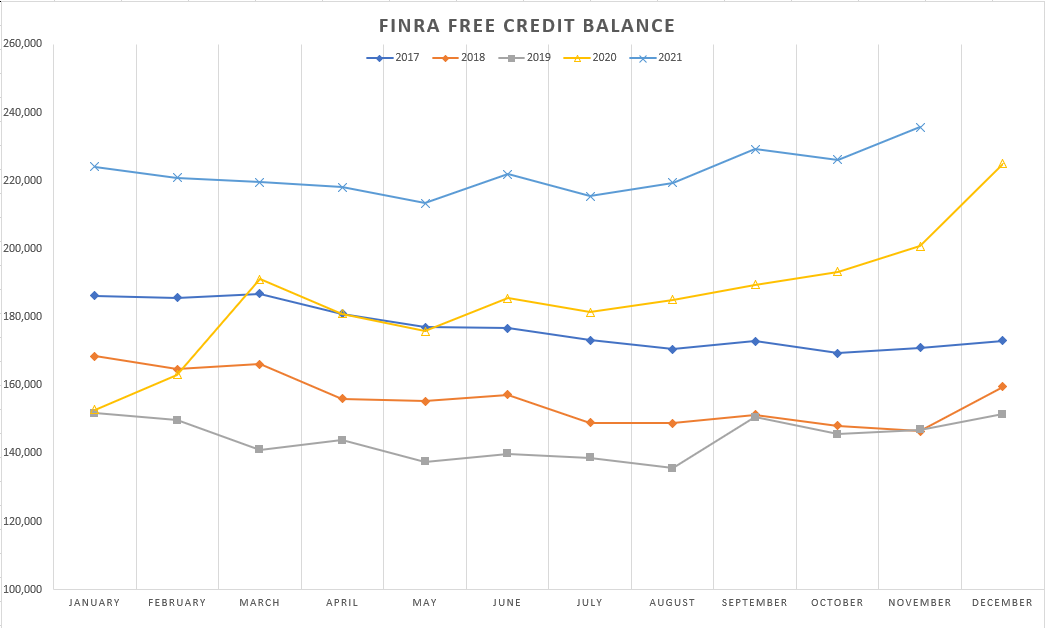

In addition to the PPI numbers, margin debt data was released yesterday. It shows that traders are holding record cash in their accounts. The Free Credit Balance is the true measure of ‘cash on the sidelines’. Investors are now holding a record $235+ billion in cash.

Pairing this with the margin debt figure provides us a glimpse into the psyche of market participants.

It appears margin debt might have peaked. November’s figure was down $17+ billion from the previous month. This isn’t as dramatic as the reduction in margin use between June and July of this year. That was almost a $38 billion reduction. Comparing this chart with the free credit balance shows that traders are reducing their highly leveraged exposure and raising cash levels.

This is a powder keg sitting on a pallet of dynamite. We are looking at a reduction of margin debt and a Fed that is increasing their reduction of market liquidity. Hopefully Jerome Powell has been good this year because he really needs Santa to come through for him.