An "inflated" mistake

Inflation data was released this week and it came in hotter than expected. The CPI came in at 3.1% y/y.

While BoA’s heatmap looks quite green (green means inflation is coming down), it is not coming down quick enough for the Fed to cut rates.

Most of mainstream press was heavily focused on the headline number (of 3.1%) because the core number was a disaster (3.9%). The higher core number reinforces the Fed’s concern that core services are going to remain sticky because of a tight labor market. I think Yahoo Finance captured the feeling well with their headline:

Today, the Producer Price Index also showed resilience, coming in above expectations.

This got me thinking about the last FOMC press conference. In it, Powell had stated that his fear of cutting rates too soon was that inflation would settle in at a higher rate than the Fed’s stated goal of 2%. This is now my base case. The popular contrarian (oxymoron, I know) view is that we will have a second wave of inflation. The TV pundits are cheering for a soft-landing situation. I get the feeling that we are going to split the difference here and force the Fed’s hand to raise rates in the fall. This will be a tricky predicament for the Fed to navigate as they will need to back the market down off the cliff edge as it is still predicting four rate cuts this year.

Getting back to popular contrarian views, I am growing weary of the RRP & BTFP noise. Every week zerohedge has to remind everyone that the RRP is draining. A key factor that they miss is that this was excess liquidity that was stored in this facility. Once it goes to zero, banks still have their deposits at the Fed.

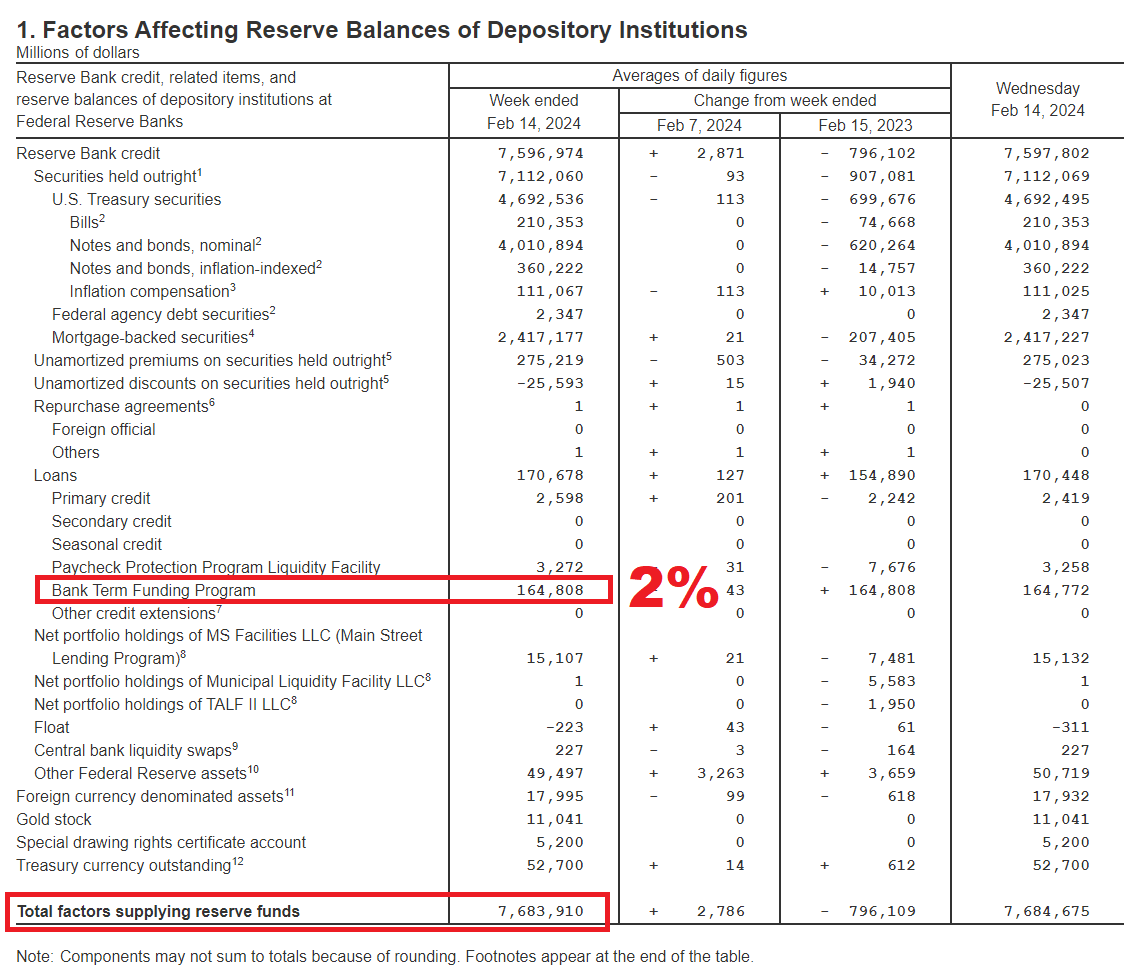

In addition, there has been much digital ink spilled about the end of the Bank Term Funding Program. Many think this will be the death kneel for regional banks. This idea is false. The Fed wants to remove the stigma around the discount window and is beginning to seed the idea into the mainstream. In addition to changing the views attached to the discount window, the BTFP program is only 2% of the total factors supplying reserve funds to the Fed.

The BTFP program is much smaller than most realize and its end should be cheered. It was a program that acted exactly like the discount window and was excessive. Now it is beginning to be abused as banks found they could borrow from the Fed and buy Tbills to eek out a few basis points return. Its end in March does not herald the apocalypse of regional banks.

US Treasury Secretary Janet Yellen came out in a press conference after the CPI report to boost markets. In her speech she said that inflation data was “a tad higher” and that the market was making a “tremendous mistake”. This announcement had red flags waving in every direction. First, the Treasury Secretary has to boost markets after a 500 point selloff? We’ve just witnessed the S&P going up for 15 of the last 16 weeks. What happens when we get a real pullback in the market? What does the White House do then? Second, the market is never wrong and always irrational. It can stay irrational much longer than you can stay solvent. This goes for you and I as well as the US Treasury. For her to say this is the height of hubris. The market has the ability to humble all and we should all be extremely concerned if the US Treasury secretary thinks she can predict what the market should and should not be doing.