An 'operation twist' by any other name

will it still smell as sweet?

O Jerome, Jerome, wherefore art thou’s Treasury Bond purchases Jerome?

The taper has been initiated and now the pace has been doubled. The Fed had and continues to concentrated their purchases of Treasuries and Mortgage-Backed Securities (MBS) at the long end of the yield curve. This means they were buying long duration bonds. This brought down that end of the yield curve causing it to be supressed.

Here is a the current view of the yield curve.

Now the Fed is letting off the gas pedal, ever so slightly. In time, this should raise interest rates on the 30-year bond. This is because the Fed is a major buyer of long-dated treasuries. Without another big pocketed market player to step in, yield will have to come up for the market to clear.

If the long end of the curve were to rise, this would cause interest rates for homes to rise and slow the real estate market. It would also begin to influence business’s expansion plans as the cost of borrowing money would rise. This would be a big brake-check for the economy.

The Fed is attempting to pump the brakes on inflation. This will act as a drag on the boom phase of the economy and may result in a recession. Something that I hadn’t considered before smacked me in the face the other day. It was the repo market and we are well past due for a review of it.

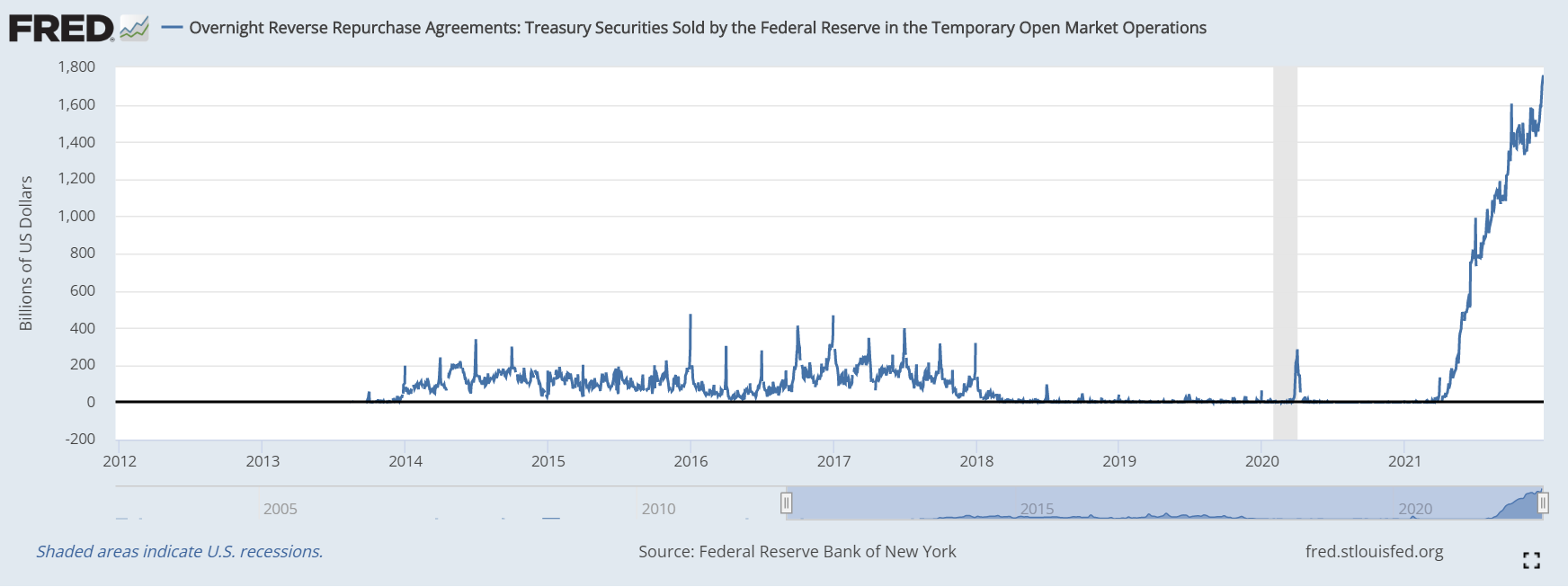

Previously, I had covered how the Fed was vacuuming up liquidity with the above average use of the reverse repo market. As a reminder, when the Fed participates in the repo market, they are buying treasuries from banks and paying them cash. In the reverse repo market, they do the opposite. They sell treasuries to banks and get paid in cash. Banks have been feeding at the reverse repo trough at excessive levels. However, when called out on it, John Williams of the NY Fed announced that the facility was “working as designed".

The reverse repo facility has continued to see record amounts of collateral purchased by banks. What I hadn’t considered before was how this was affecting the yield curve. By buying the long-end of the curve and selling the short-end, the Fed is essentially aiding in it’s flattening. They have artificially lowered long duration rates and raised short duration bonds.

The Fed has done this before. They called it Operation Twist. Mish covered this idea a few days ago. I’m curious though. What if, by the Fed’s actions in the reverse repo market, they have set an artificial floor for short-term rates. Would the yield curve still need to invert to signal a recession was coming?

The 10-year treasury minus the 2-year has been stopped in it’s tracks. It has found a tight range with which to trade in. It has oscillated between 0.84% and 0.75% since the beginning of the month. Is it being prevented from going lower by the Fed’s actions in the reverse repo market?