Back to the grind

the grind higher in the S&P that is

What a way to come back from vacation. We’ve got some data to get through but first I want to address the delta variant. It looks like many states are starting to hit their peak of cases and hospitalizations.

This is good for oil and the general stock market. Oil is still stuck in a short-term bear market.

Crude oil peaked in July at $75/bbl. Since then, it has been discovering new lows and lower highs. This is what I mean by a short-term bear market. Short-term, to me, means 3 months or less. On the long-term picture (6 mo to 1 year), oil is in a bull market. As long as we can stay away from vaccine passports (or other such nonsense) the picture looks bright for people and products to travel. This means more oil consumption. My source tells me the ports are absolute chaos right now. We’ve got big backups all along the west coast. Also, the ports in China are slow due to the restrictive lockdowns. Once the restrictions are lifted and people are put back to work, these shipping bottlenecks will ease. It will take time to move through the backlog. We could be looking at several months before the ports clean up their act.

On the economic news front, we saw the release of home price data. I’m a big fan of using the home price data as a proxy for inflation. In Robert Shiller’s book, Irrational Exuberance, he came to the conclusion that long term trends in home prices had no relation to changes in construction costs, interest rates, or population but that the difference in prices can be explained by inflation. He then paired up with economist Karl Case to create an index to track the repeat sales of the same homes.

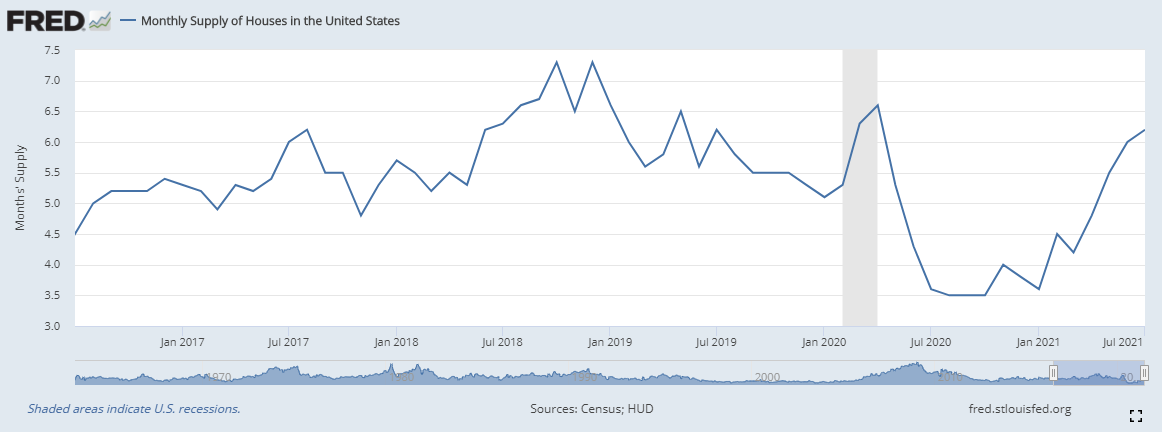

Above is the current data from the index created by Robert Shiller and Karl Case (the case-shiller home price index). It has hit a new high of 18.6% on a year-over-year basis. Something to keep in mind is that this index is two-months behind. They posted the June data on August 31st. Since June, things in the housing market have changed. We have seen the monthly housing inventory move higher and housing staying on the market longer.

To me, the Case-Shiller home price index is a lagging indicator of inflation. Also, I believe that there is another factor pushing housing prices higher than pure inflation. That factor is FOMO, the fear of missing out. People have been moving out of the cities to greener pastures. There was a big exodus as people realized they didn’t like getting locked-down in a tiny apartment in a big city. So they moved to where they could afford a house and some space. Tele-commuting aided in their ability to live anywhere. We are now seeing the dust settle. I believe, in time, we’ll see the Case-Shiller index come down to better reflect inflation but for now, it seems dis-jointed from reality. I believe we are seeing high inflation, but I don’t believe we are seeing inflation as high as 18.6%. In time, housing costs will begin to push on the CPI/PCE inflation figures. Then we’ll see what kind of jawboning the Fed can do to keep commodity prices down.

Today saw the release of the ADP employment figures. While employment is increasing, it was a serious disappointment to the experts.

The expert consensus was growth by 613k jobs. The actual change was 374k. The general market was unfazed by the report. Nela Richardson, the ADP chief economist had this to say about the report:

“We have seen a decline in new hires, following significant job growth from the first half of the year. Despite the slowdown, job gains are approaching 4 million this year, yet still 7 million jobs short of the pre-COVID-19 levels. Service providers continue to lead growth, although the Delta variant create uncertainty for this sector.”

I am still of the mind that many on the pandemic assistance dole will wait until the last moment before beginning the search for a job. September should see a big boost in the employment figures with the ending of the relief. I expect that October and November will be real hot months for inflation and the stock market as job vacancies are filled and money from higher wage rates is put into the hands of consumers. My two concerns are the Biden administration shooting itself in the foot or a resurgence of the coronavirus. Either of these wild cards could spell disaster for investors.