Consumer credit blowout

and the jobs report; expected vs actual

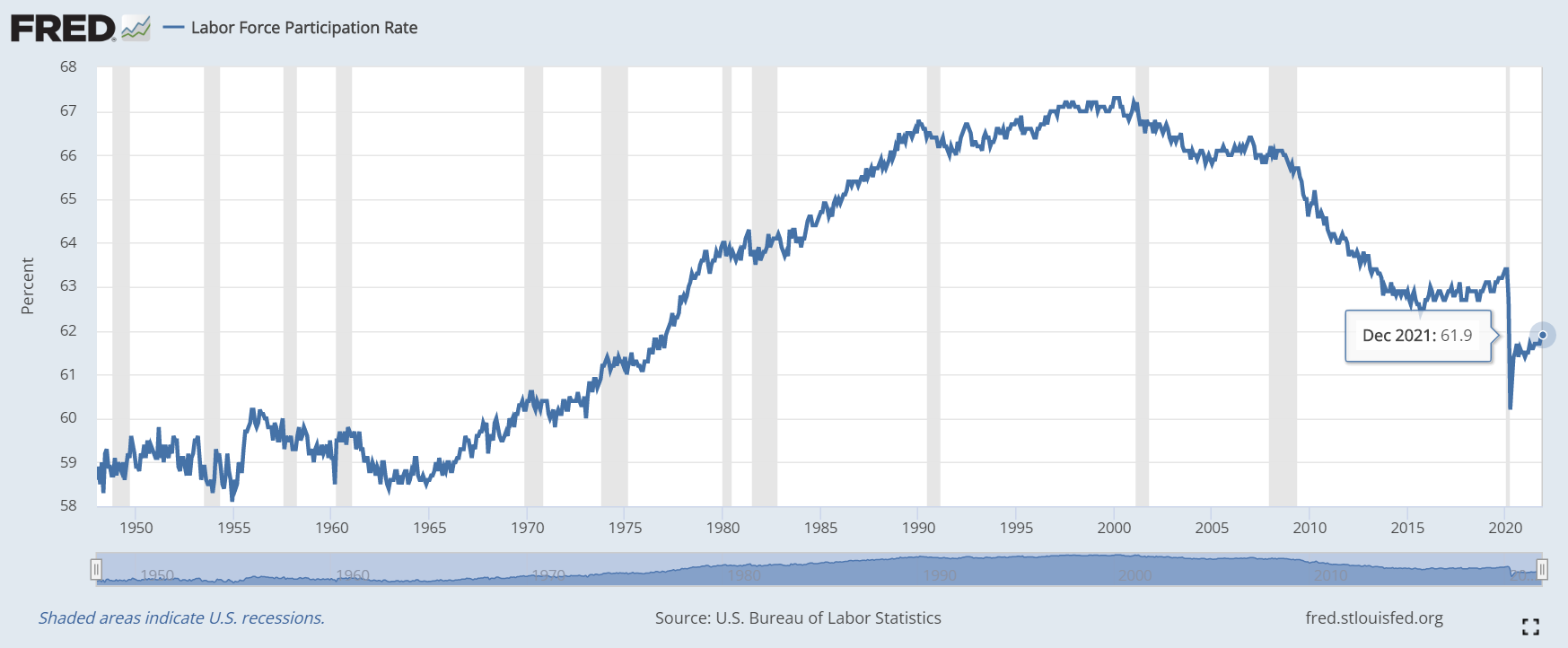

The unemployment rate is what the Biden administration and the financial talking heads are all excited about today. It has hit a low of 3.9%. Here is the historical picture.

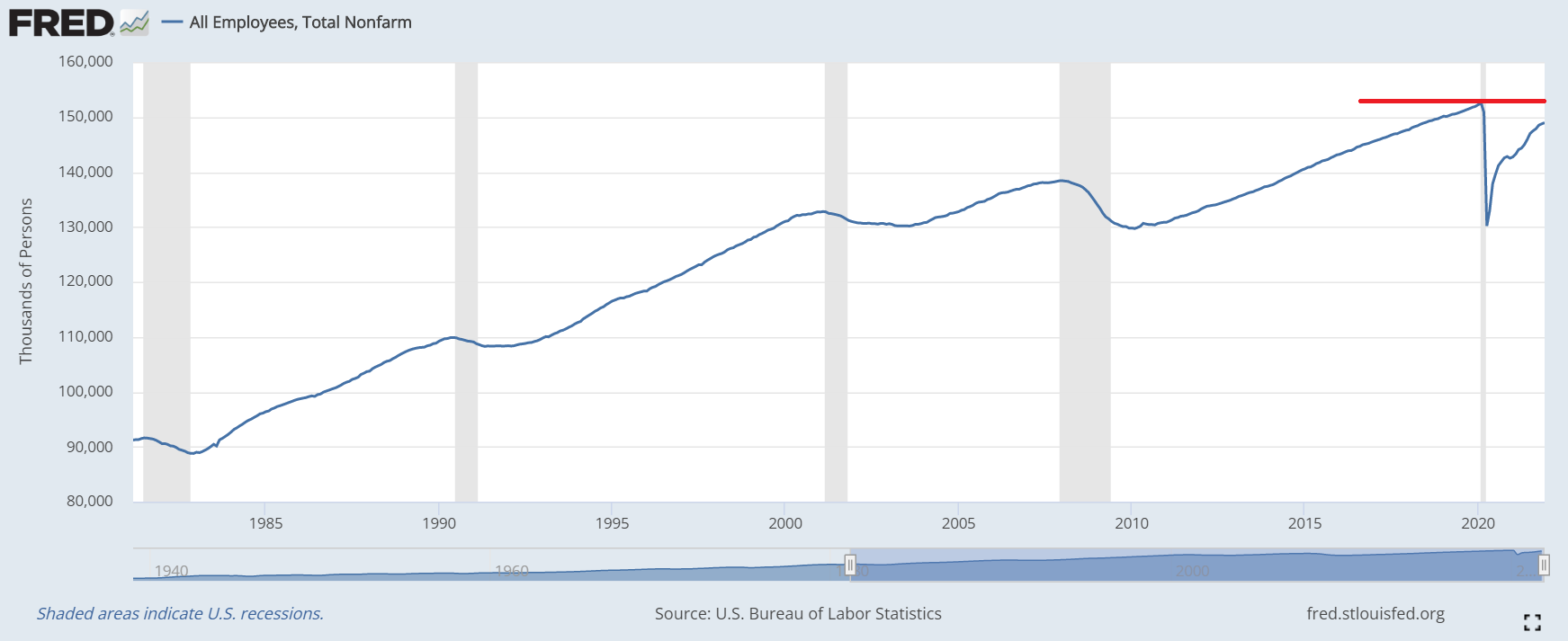

3.9%! the talking heads exclaim. Words and phrases like unprecedented and amazing recovery are on their lips but they are missing the bigger picture here. The jobs report showed less than half of what was expected. Also, the total employees figure is still below the previous cycle’s high.

This indicates that people are leaving the workforce. In addition, a 3.9% unemployment rate is typically the bottom of the boom-bust cycle. Look at the above graph and you’ll see. Once this kind of low is hit, a recession followed. The sole exception could be the early-to-mid 1950s where unemployment continued to spiral lower. I don’t want to discount the possibility that it continues to muddle along. In fact, I expect it to. This also means that employers are going to get increasingly desperate for workers. At 3.9% unemployment, there aren’t many left to hire.

We are ripe for a policy error from the Fed because they are looking the wrong way while crossing the street. They are focused on the participation rate while everything else says this economy is about to hit the wall.

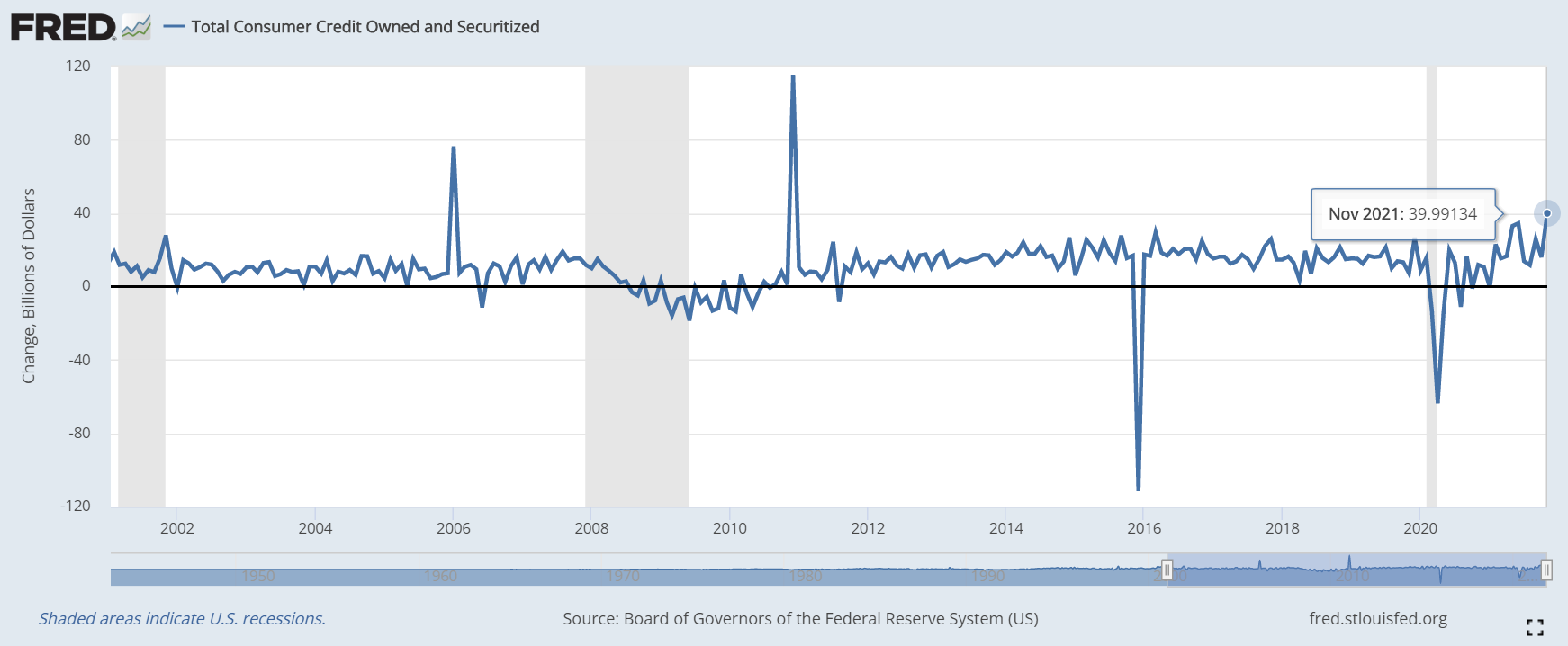

The big one that stood out to me today was the consumer credit numbers.

Total consumer credit jumped nearly $40 billion in November. This blew out the estimates of $20 billion. Consumers are borrowing money to keep up with their current lifestyle.

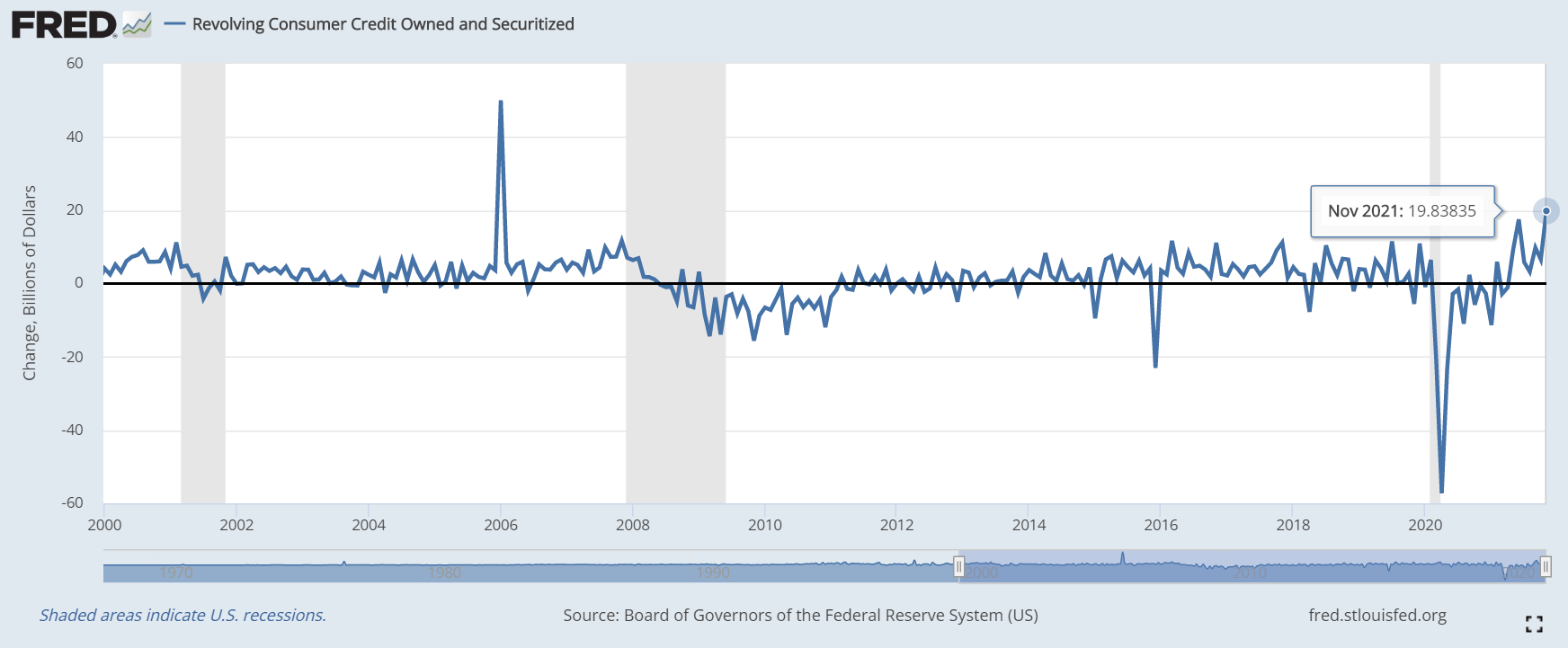

Revolving credit was the big mover.

A quick note about revolving vs non-revolving credit. Revolving credit includes credit cards, home equity lines of credit, and personal lines of credit. It is considered revolving because the payment can change from month-to-month depending on the balance. Non-revolving credit is a loan with a set monthly payment and a set pay-off date. Things like home mortgage loans, car loans, and student loans.

This is one of the biggest rises in revolving credit use. With this big rise, we can come to the conclusion that the American consumer has tapped all their “sunny day” funds and is now trying to stay ahead of inflation by using plastic instead of savings. With consumers looking tapped out, the economy will be ever more reliant on the Fed’s money printers to keep it afloat.