Credit vs Equities

and a portfolio update

There has been a serious yield compression across asset classes. A graph has been floating around twitter showing the compression between the S&P500 earnings yield, investment grade bonds, and short-term treasuries.

This kind of squeeze is rare. What it means is that you can take on less risk in the credit or treasury market and get a similar return to a higher risk asset class (common stocks). Let me define this further.

When you buy a bond, it is a contract with a borrower where you lend them money at a fixed rate with the expectation of the principle being returned to you on a fixed date. There are many examples. US Treasury bonds are known as the “risk-free” rate. These are often thought of as the lowest risk. CDs (certificates of deposit) are also very low on the risk scale and are a kind of bond.

Slightly higher on the risk scale would be investment grade bonds. These would be contracts with companies that are deemed to be low risk due to manageable levels of debt, good earnings potential, and have a track record of paying their debts. The riskiest bonds would be those that are below investment grade, also known as high yield bonds or junk bonds. These would be companies that have a questionable track record of paying off debt, or have variable (or negative) earnings potential.

The highest risk would be equity in a company. This is because creditors get paid first in bankruptcy court and those that hold equity (or stock) in a company get paid last. Equity is also high risk as it is often highly volatile. Stocks go up and down for a variety of reasons. We can and do have 10%+ swings in some stocks over a series of days or weeks. This is not the case in the credit market.

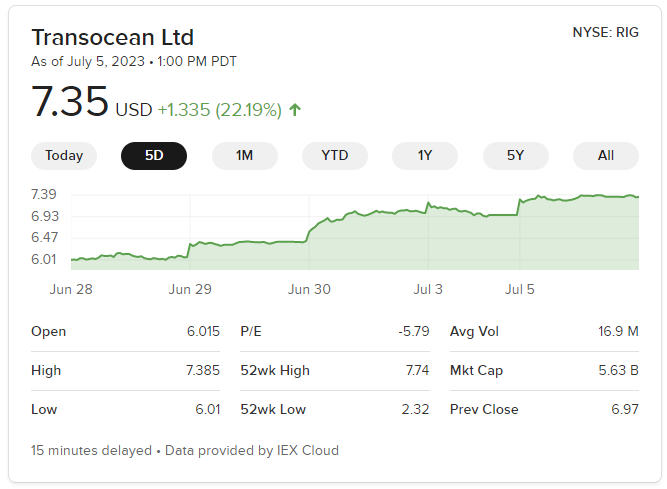

This is just a recent example of a stock that swung 22%+ in a matter of 5 days. You do not see this kind of action in the bond market.

Recently Howard Marks (Co-Chairman of Oaktree) and David Rosenberg (Co-Portfolio Manager, US High-Yield, Global High-Yield, and Global Credit) had a conversation about the credit market. It was highly insightful and certainly worth the half-hour. The biggest take-away for me is that we are in something of a credit buyer’s market. We are witnessing a time period where yields are high and quality of issues is high. In addition, high-yield debt is seeing some of the shortest maturities on record.

This all combines and leads to a boom in private credit.

Private credit is a lot like private equity. Private equity is an investment fund which invests in and restructures private companies. Private credit is an investment fund which loans money to companies. It has really taken off in recent years and I expect this trend to continue.

We are also seeing all the major Wall Street players get in on the act.

“Blackstone Inc. popularized the concept of a non-traded private-credit product for Main Street in 2020, with a fund that has grown to manage $48 billion of assets, including leverage, as of April 30. Blue Owl Capital Inc., Ares Management Corp. and Fidelity Investments, among others, have created similar funds.”

Portfolio Update

The yield compression and expansion of private credit have motivated me to search through the credit market for good issues to invest in. I’m still going through that process but I’ve added one issue in particular to my portfolio.