Crypto, the SEC, and how to fleece sheep

and the relationship between liquidity and the stock market

It seems the big guys are dipping their toes into the crypto-sphere. It was announced that Blackrock will be creating an ETF that would track bitcoin.

BlackRock (BLK.N), the world's biggest asset manager, on Thursday filed for a bitcoin exchange-traded fund (ETF) that would allow investors to get exposure to the cryptocurrency, as the asset class comes under intense regulatory scrutiny.

BlackRock's iShares Bitcoin Trust will use Coinbase Custody as its custodian, according to a filing with the U.S. Securities and Exchange Commission (SEC). The U.S. regulator has yet to approve any applications for spot bitcoin ETFs.

This comes at a very interesting time for crypto-based assets. Coinbase and Binance are both feeling the heat from the SEC. The SEC sued Coinbase for operating as an unregistered securities exchange, broker, and clearing agency. One day prior, the SEC filed charges against Binance for co-mingling client funds. A big no-no.

While on the surface it seems that these charges are warranted, the timing is very suspect. I find it interesting that while the SEC goes after the pioneers in the bitcoin exchange industry, the big wall street players begin to setup the fleecing stations for investors.

The other thing that is interesting about the timing is that bitcoin is expected to halve within the next year. Halving can be a volatile time for bitcoin.

As a general rule of economics, lower supply, and steady demand should mean higher prices. The price of bitcoin experiences the biggest runs usually before halving since it decreases supply while keeping demand high.

It is important to note that demand does not necessarily equate to an increase in price or even a stagnation in price. It has been several years since the last Halving of the cryptocurrency market took place in 2016, and there are now more cryptocurrencies competing for users’ attention.

Experts predict that Bitcoin’s value could fall significantly if it halved in 2024.

Now I don’t have a dog in this fight. I don’t own any bitcoin and my views are mixed on its actual value and function. Value is subjective. This is not a sell recommendation nor a buying recommendation. It is simply a warning that when I see big wall street players flock to something, I know that I should be running in the opposite direction.

Earlier in the week I saw an interesting tweet. Then just yesterday, Dan asked me about the story in marketwatch that followed up on this idea.

Here is the tweet:

Torsten Slok, the chief economist at Apollo Global Management, put together the above comparison. He had this to say about it:

“Since SVB collapsed, the Fed has been adding liquidity, and the S&P 500 is up more than 10%. The high correlation between Fed net QE and the S&P 500 seen in the chart below suggests that Fed liquidity is a crucial driver of the stock market.”

I attempted to recreate the above chart. Here is what I came up with:

I substituted the Wilshire total market cap for the S&P500. I also had to adjust the index to get the charts to track. Even with those adjustments, the chart doesn’t track all that well. Torsten’s original chart above only showed 3 years’ worth of data. I always prefer a longer-term horizon on these kinds of things. With all these things in mind, I do believe that Torsten is on to something but it is something Robert Wenzel was on top of for a long time. It is the idea that Fed liquidity moves markets which is an idea that I believe has been proven true over time.

The struggle is finding the best way to monitor the money the Fed injects into (or withdrawls from) the economy and the lag that might take place when that action happens.

I think the best way to look at this is that the Fed always in the process of propping up the banks. The banks put these funds the Fed gives them to use and this money finds its way into the capital markets. The Fed is known as the lender of last resort. Theoretically banks should be lending to each other and the Fed only needs to step in when they don’t. In practice, the Fed is a constant lender to the banking system. So when the Fed pulls back the liquidity punch-bowl the credit markets seize up as the banks will refuse to lend to one another. The Bank Term Funding Program (BTFP), Other Credit Extensions (OCE), and the Repurchase Agreement (REPO) facilities are all providing liquidity to the banks and therefore the market. If the use of these credit facilities dries up or the Fed reduces their participation levels in the facilities, liquidity for the banks will dry up, which will cause assets to reprice lower.

It takes only a small fluctuation in the economy to produce a large fluctuation in the availability of credit, with great impact on asset prices and back on the economy itself.

-Howard Marks (You cant predict. You can prepare. Nov 2001)

Marks' quote is from a note he wrote in 2001 and it references the availability of credit. While ‘01 saw a healthy credit crunch, ‘08 was magnitudes worse. The key here is, is credit available for banks? If financing is plentiful and easily obtained, the capital markets flourish but if financing is constrained, assets will get repriced lower. Bear in mind that the ability to get financing can go from easily obtained to impossible to secure in an instant.

Financial institutions have a special reliance on credit markets. They are in the business of trading money. They typically need financing to keep that business going. Earlier I said that the Fed was the lender of last resort. So where do banks get their funding if not the Fed? The credit market and deposits. Right now, the credit market is going through a period of transition.

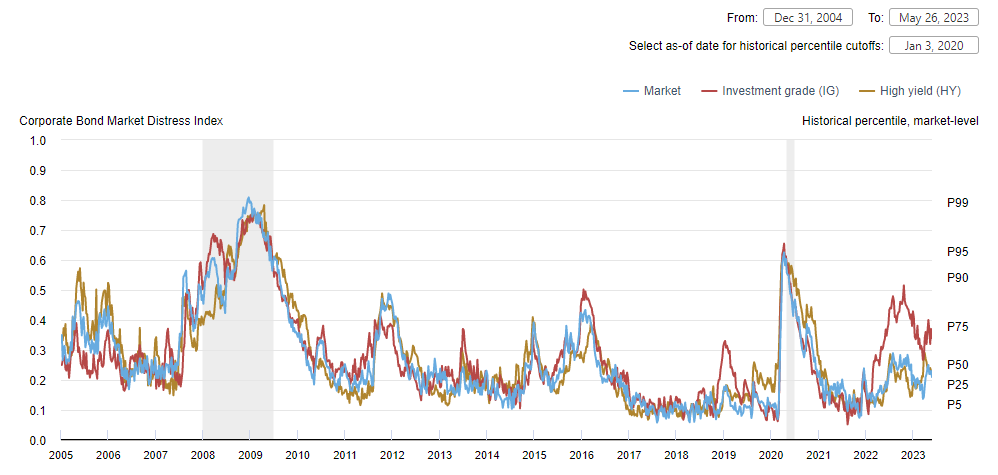

Investment grade bonds are seeing significant stress and a lot of these bonds are for financial institutions.

Bond investors are worried the banks. Deposit flight, commercial real-estate exposure, and hold to maturity loan portfolios are all heavily weighing upon the sector right now. If liquidity does dry-up, stock valuations will matter.

Excellent response, sir!. FED givith and the FED taketh!