Employment, credit, and a double dip

An early indicator that a recession is coming is the 10-year treasury minus the 2-year treasury. Earlier this year it went negative. Now it has double-dipped and gone negative again.

Yesterday it was at -4 basis points. Today it finished at -2.

A double dip like this is common. It has happened 3 out of the last 4 recessions:

1989 went negative twice. Then it went negative again at the beginning of 1990 prior to the recession (a triple dip!).

The curve inverted in ‘98 and then again in 2000 before the tech bubble burst.

The curve went negative in ‘06 and then again at the end of ‘06 through the beginning of ‘07. Afterwards, we experienced the housing crash.

However, the markets continue to shrug this off and churn higher.

I believe there are two forces at work here. The first is that the dollar is gaining strength. With the dollar rising against the euro, yen, and pound, it has attracted capital. Capital is fleeing foreign markets for the “safety” of the dollar and US markets. This has caused the strange levitation we are seeing right now.

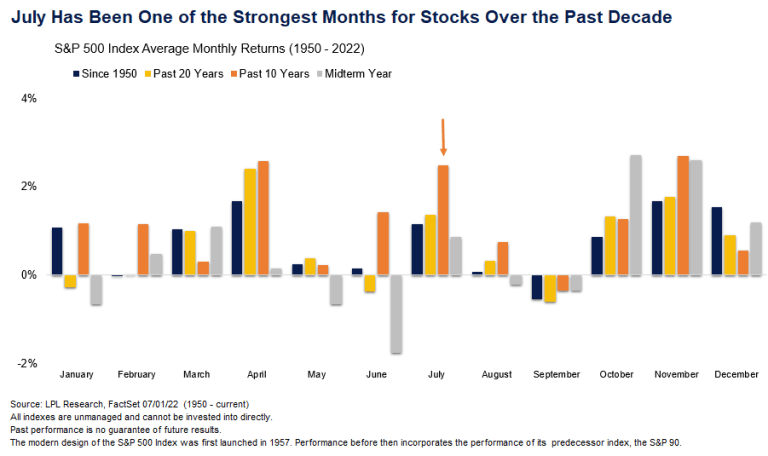

The second factor that plays into the levitation act that the market is performing is that July is consistently a strong month for stocks.

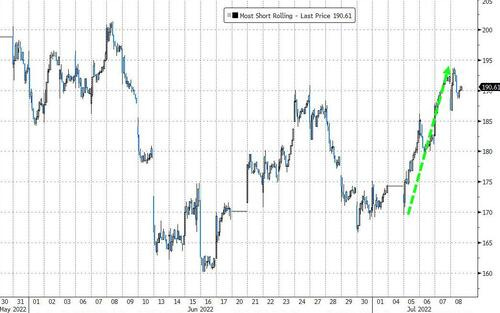

All the big banks believe a market crash is at hand, so the market takes the other side of that trade to cause the most pain. Traders got out over their skis on this one and now are closing out their shorts. You see this is the “most-shorted” stocks getting pushed higher.

Today saw the release of employment data. The big number was non-farm payrolls surprising to the upside. The US economy added 372k to the payrolls in June. This beat the forecast of 268k. This continues to point at an extremely tight labor market where employees are in the driver seat bidding up wages.

The average hourly wage continues to climb, however, it is still losing ground to the CPI. Still, it is another factor pointing towards a tight labor market.

With today’s report, the unemployment rate was released and it is on par with the bottom of previous cycles.

At 3.6%, it is the lowest unemployment rate since 1969 with the exception of Sept 2019 and Jan-Feb 2020 where the rate hit 3.5%.

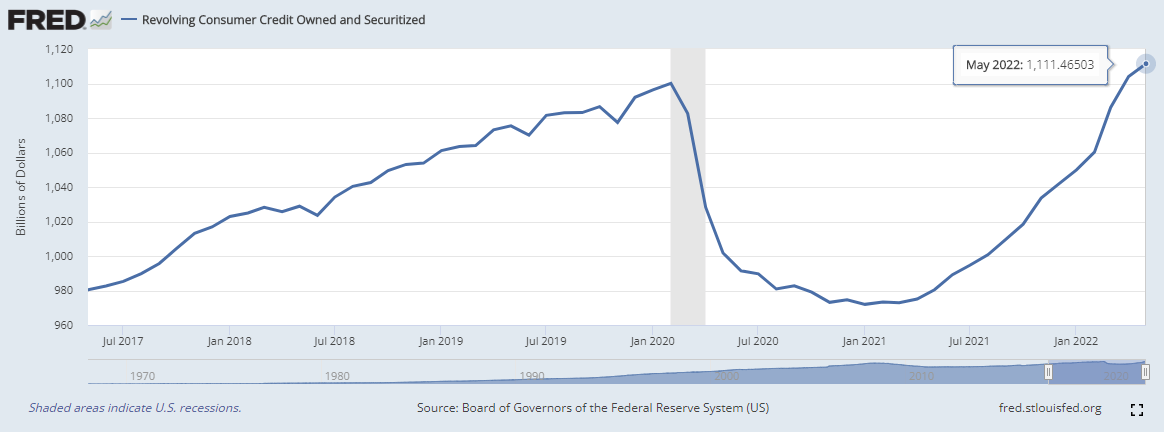

Today also saw the release of the consumer credit figures. Revolving credit has continued to push higher.

We’ve now exceeded the pre-lockdown high for revolving credit for two consecutive months. Total credit also climbed 7.3% year-over-year.

It is difficult to watch the market get bid up. Shorts are getting covered and retail is continuing to pile in. I know that this can’t last and I wonder what exactly is getting priced in.