Fed ends forward guidance and replaces it

With forward guidance

Jerome Powell turning off forward guidance circa July 2022.

Powell and company terminated the idea of FOMC forward guidance. What is forward guidance? Straight from the Fed.

https://www.federalreserve.gov/faqs/what-is-forward-guidance-how-is-it-used-in-the-federal-reserve-monetary-policy.htm

What is forward guidance, and how is it used in the Federal Reserve's monetary policy?

Forward guidance is a tool that central banks use to provide communication to the public about the likely future course of monetary policy. When central banks provide forward guidance, individuals and businesses will use this information in making decisions about spending and investments. Thus, forward guidance about future policy can influence financial and economic conditions today.

The Federal Open Market Committee (FOMC) began using forward guidance in its postmeeting statements in the early 2000s.

The Fed has replaced forward guidance following the FOMC meetings to using speeches by Fed members to relay what the Fed's expectations are. This past week we had four Fed officials making public comments. First up was Michelle Bowman.

https://www.federalreserve.gov/newsevents/speech/bowman20220806a.htm

Based on current economic conditions and the outlook I just described, I supported the FOMC's decision last week to raise the federal funds rate another 75 basis points. I also support the Committee's view that "ongoing increases" would be appropriate at coming meetings. My view is that similarly-sized increases should be on the table until we see inflation declining in a consistent, meaningful, and lasting way.

Ms Bowman also perfectly illustrated the reason the Fed ditched the forward guidance protocol.

On the subject of forward guidance, I am pleased to see that following the July meeting, the FOMC ended the practice of providing specific forward guidance in our post-meeting communications. I believe that the overly specific forward guidance implemented at the December 2020 FOMC meeting requiring "substantial further progress" unnecessarily limited the Committee's actions in beginning the removal of accommodation later in 2021. In my view, that, combined with data revisions that were directly relevant to our decision making, led to a delay in taking action to address rising inflation.

The Fed doesn't want to have their hands tied by the forward guidance they've given in the past because the future is uncertain. They are anticipating the need to make a quick change if the economy deteriorates quicker than they expect.

Next up is Esther George, the Fed President of the Kansas City branch.

https://www.yahoo.com/lifestyle/feds-george-says-pace-endpoint-180202617.html

"To know where that stopping point is ... we are going to have to be completely convinced that (inflation) number is coming down."

Kashkari then threw in his two cents.

https://www.reuters.com/markets/us/fed-must-get-inflation-down-urgently-kashkari-says-2022-08-18/

"We need to get inflation down urgently."

And finally today Federal Reserve Bank of Richmond President Thomas Barkin said

https://finance.yahoo.com/news/fed-barkin-says-central-bank-153652205.html

“We’re committed to returning inflation to our 2% target and we’ll do what it takes to get there.

There’s a path to getting inflation under control but a recession could happen in the process.”

This is a united front from the Fed. They are committed to controlling inflation and if it causes a recession, so be it. This should be a signal to investors that the pivot in policy is a long ways off yet talking heads like Jim Cramer continue to urge retail investors to go all in.

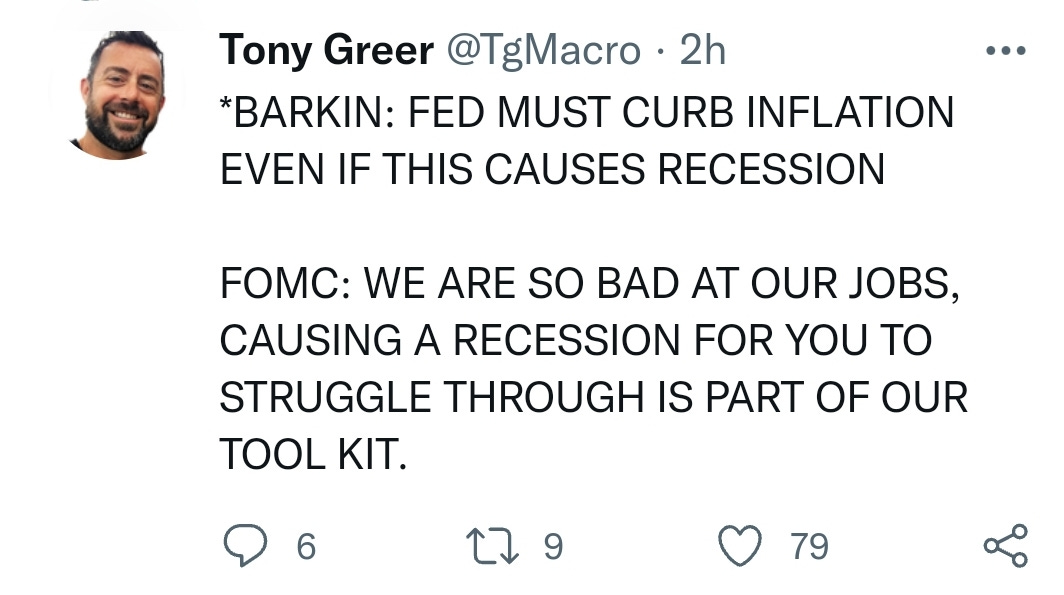

Tony Greer put it best:

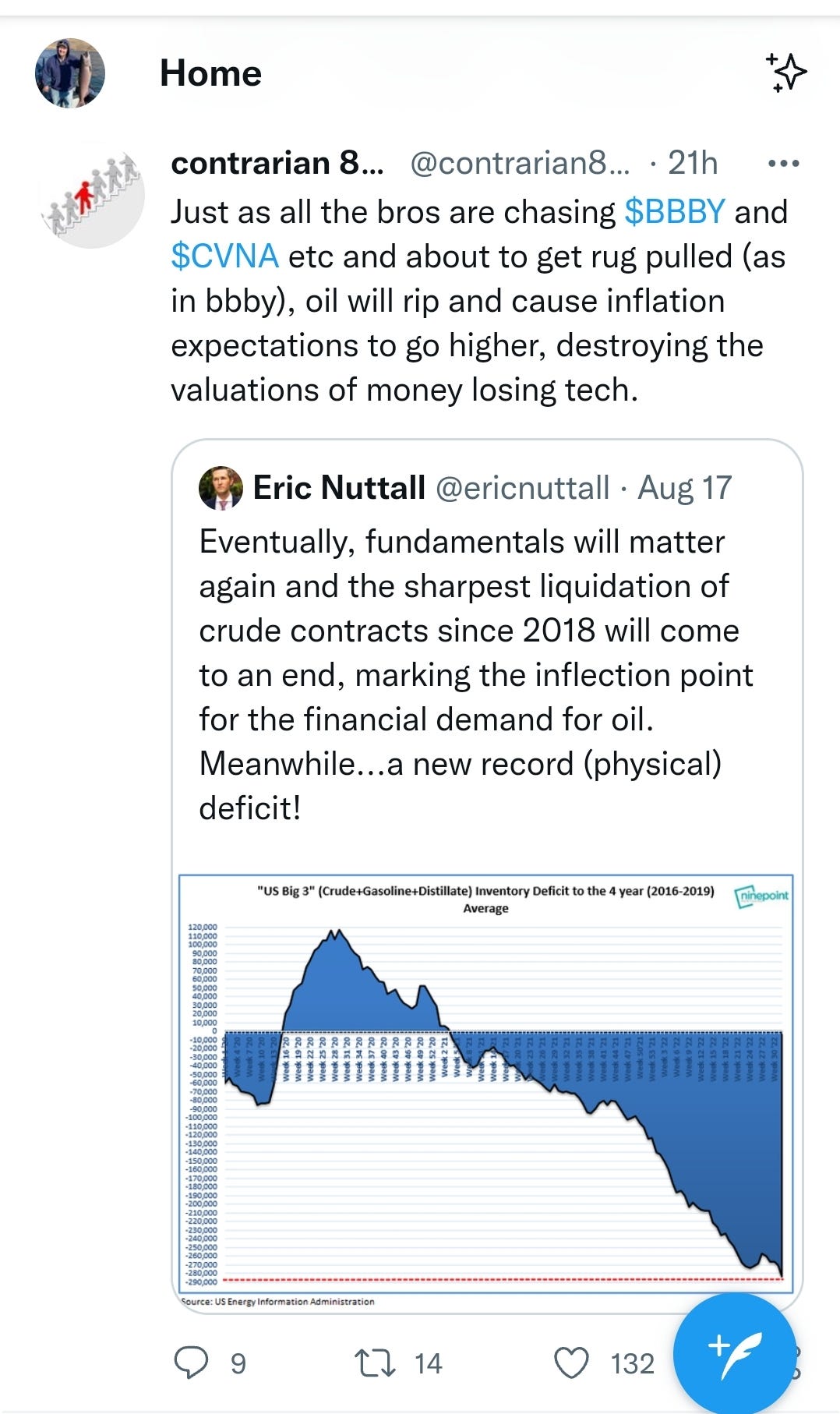

The last word for the week comes from twitter user @contrarian8888 who posted this yesterday:

Is it appropriate yet to be concerned that the Fed might usher in a depression?