I'm back baby!

and advice for those who are risk-oriented.

With all the dismal economic news coming out, it is hard to be excited about being invested in the market right now.

Tuesday saw the release of the retail sales data. Bank of America had put out a preview that looked downright terrible. They are able to accurately predict retail sales data because of their large credit card customer base. They get to have, practically, real-time data on the health on the consumer. Since the stimulus gravy train has ended, retail sales have been in for a correction. The consensus was a -0.3% reduction in month-over-month data but the actual results were -1.1%. Ouch. Below is the year-over-year percentage change in advance retail sales.

As you can see, that stimulus money really juiced the numbers for a short period of time. Now that the stimulus has ended, we are going to experience the hangover.

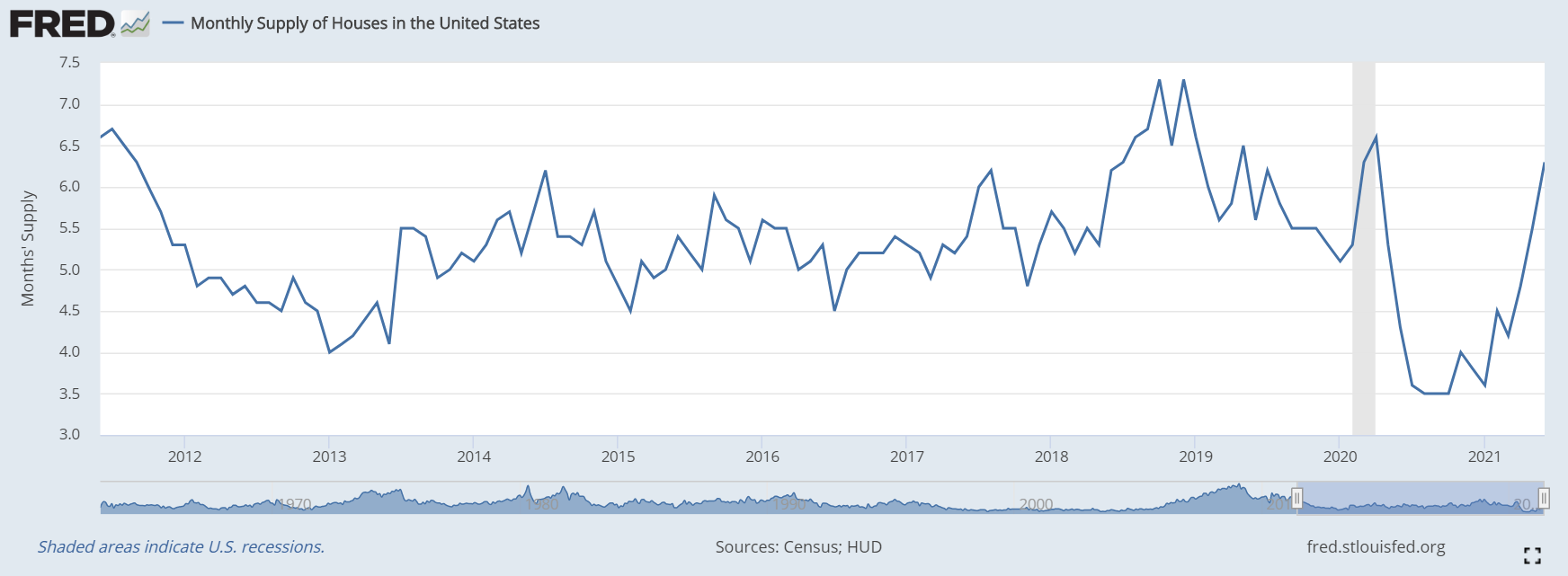

Wednesday saw mortgage, housing, and building permit data released. The most concerning of these three was the housing starts. They were down -7%. Big Ouch. The good news is that we have rebounded from the pandemic shutdown lows to the long-term housing starts average.

From my own observations of the housing market, it seems the buying frenzy has slowed way down. I am seeing inventory return to normal levels.

The monthly supply of house data was last updated on July 26th. It is updated monthly, with the next release happening on August 24th.

Wednesday also saw the release of the FOMC minutes. As a regular consumer of these snooze inducing tomes, I would have assumed that the market had already priced in the idea that the Fed was hinting at, thinking about, discussing, the possibility of talking about tapering but I would have been wrong. Wednesday saw a brutal and swift correction at the end of the trading day. While the financial news media was caught up in the taper talk, a little nugget of information slipped past their notice. Within the minutes the manager of the Fed’s open market operations, Lorie Logan, was concerned about the reverse repo facility (RRP). The RRP has been a hot topic as it’s use has exploded recently. Ms. Logan is concerned that users of the facility are reaching their limits on its use and if a crisis were to emerge, these users wouldn’t be able to utilize the facility.

“if a number of counterparties reached the per-counterparty limit on their ON RRP investments and downward pressure on overnight rates emerged, it may become appropriate to lift the limit.”

The current limit of $80 billion was instituted in mid-March. The previous limit was $30 billion. The Fed just got an economics lesson. When you subsidize the use of the RRP facility by paying interest on its use, more use of the facility will follow.

Finally, I have tighten up all my stops. My stops are now 7-8% below current market prices. I advise you all to do the same. In fact, risk-oriented traders should consider going short. We are treading in dangerous waters right now. The market got caught off-guard by the taper talk and the Jackson Hole symposium is next week. All ears will be listening closely to Chairman Jerome Powell for further taper talk. I feel we have a legitimate chance of a policy announcement error. Another reason to tighten up the stops is this:

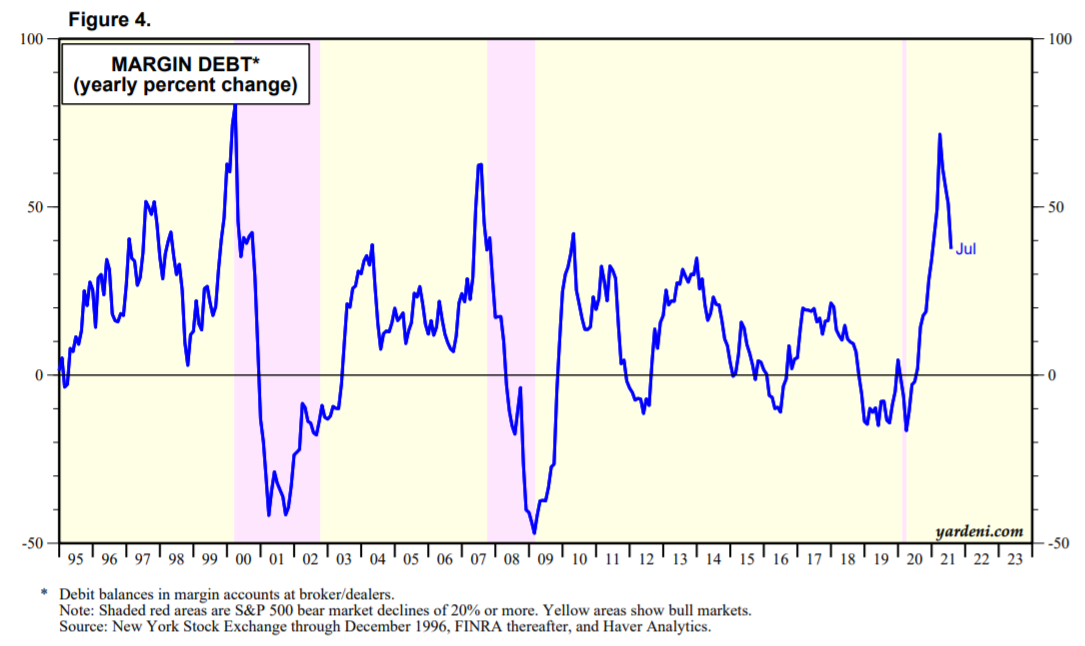

We have seen a dramatic reduction in the use of margin debt. Margin debt is when traders use their stocks as collateral for loans to buy more stocks. Sharp corrections in margin debt use have historically lead to market corrections. It is a real shame that the Fed doesn’t release the H.6 money stock reports weekly any more. This would give us a better picture of the severity of a correction. Thankfully it gets released next week Tuesday. Hopefully it will give us a clearer picture of the market’s recent turbulence.