Inflation and Powell's congressional testimony

Inflation data was posted this past week. The Consumer Price Index was posted on Thursday and the Producer Price Index was released on Friday.

The Consumer Price Index came in at 3.0% and core came in at 3.3% with the PPI at 2.6% and PPI finished goods at 1.4%. This was seen as very bullish for a rate cut and investors took notice and rotated away from the MAG7 and into smaller cap stocks.

BoA’s heatmap gives a better detail on what is going on under the hood.

It is now very obvious that shelter costs are holding up lower inflation readings.

At 5%+ y/y, shelter seems to be the only factor holding up core CPI.

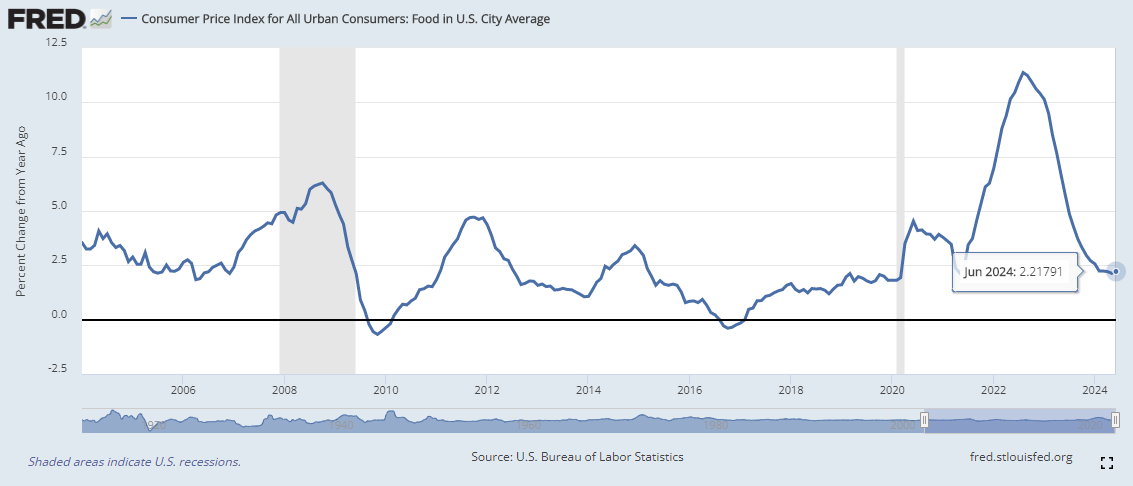

As far as the headline number goes, food seems to have bottomed here.

While I wish food costs would continue to go down, the above is not a chart I would short. It certainly looks like it is making a bottom here at 2%. In addition, gas prices look to have bottomed at the beginning of the year and are refusing to retest that level.

These factors continue to weigh on the Fed’s long-term decision making capabilities. The market, however, takes a much shorter viewpoint on all of this.

After the inflation data hit, the market immediately began pricing in 6 rate cuts in the next 12 months with the first starting in September. I’m not sure this is what “higher for longer” means.

Fed chair Jerome Powell sat down in front of lawmakers this past week and it gave them a great opportunity to drill further down into what higher for longer might mean, what amount of greater confidence the Fed might feel is necessary before cutting rates, or the benefit of higher rates on the economy. Unforunately, 99% of the time was spent attempting to garner political points. The senatorial hearing was a waste of time but there was a brief moment during the testimony in front of the house where Powell spoke to the balancing act that the Fed finds itself in.

At roughly 1:16:30 Powell states,

“We want to have greater confidence. That means more good inflation readings that inflation is moving sustainably down to 2%. Remember, we have a dual mandate, too. We are not just an inflation targeting central bank. We also have an employment mandate. So I could also see us cutting and we’ve said this, I’ve said this, if we saw unexpected weakening in the labor market. And we do now see, I’ll speak for myself, I now see the risks to the two mandates being much closer to being in balance. I think for a long time we’ve had to focus heavily on the inflation mandate. I think now we’re getting to the palce where the labor market is getting pretty much in balance to where it needs to be. So now we are looking at both sides (of the mandate).

*bold is mine*

This piggybacks on the Senate committee testimony where Powell had indicated that the Fed has seen one “good” inflation data point and one “ok” data point but that inflation and the labor market had both “cooled significantly”. This seemed like a great opportunity to gain a better understanding of how the Fed feels about the current rate environment that it finds itself in but alas political points were deemed more important at the time. Maybe the Economic Club of DC will have a better conversation with Powell when he sits down with them on Monday. I’m also looking forward to Governor Chris Waller speaking at the Kansas City Fed on the Economic Outlook on Wednesday.