Inflation vs Deflation

The greatest match-up of all time?

User Matt posted the below question last week.

Hi Alan, curious about your thoughts regarding the inflation vs. deflation debate I am seeing crop up more often across the financial crowd I follow (e.g., Zerohedge, Mish, Doomberg, Quoth the Raven, etc.). The deflation crowd continues to point to the decreasing bond market rates as a sign inflation concerns are overblown. My quick take is bond traders haven't experienced this type of economic environment and thus don't know how to trade in it so we can't put much stock in what that is telling us. If it's easier feel free to respond in a post. I posted this same question to David B on his substack. Thanks in advance!

I’m always up for a good debate and I’m no stranger to having to defend my position but let’s lay out the terms of this fight as they have evolved over time.

Inflation, noun; a persistent increase in the level of consumer prices or a persistent decline in the purchasing power of money.

Deflation, noun; a persistent decrease in the level of consumer prices or a persistent increase in the purchasing power of money.

These are the common definitions of the day. The Austrian perspective is that inflation is an increase in the supply of money which dilutes the purchasing power of existing money. Deflation would be the opposite. This is a more technical answer. The challenge for Austrians in the investing world is accounting for other causes of deflation that fall outside of this definition.

Deflation has been the heavyweight champion for the past 40 years. He has defended his title many times (the early 90s, 00-02, 07-08). His one-two combo of the globalization of supply chains and technological advancements have been hay-makers to his opponent.

When supply chains went global, manufacturers were able to reduce their bottom line. This means that companies were able to produce roughly the same quality of goods that their customers expected but at a reduced cost. More companies began seeing the benefit to expanding their supply chains overseas. In time this led to falling prices as competition heated up.

In addition to the supply chain expansion, technological advancements have aided in the ability of businesses to reduce costs. The advancement of computing technologies has been a tremendous factor in lowering costs across the board. It has also made existing ideas much more efficient. An example would be just-in-time-inventory. This was a method pioneered by Toyota in the 1970s. It didn’t take off in popularity until the 1990s. This was because computers could now do the work of an entire accounting division. Walmart truly perfected the practice by integrating their point-of-sale cash registers with their inventory monitoring computers. This allowed them to streamlined their reorder process and monitor changes in consumer behavior. By increasing the amount of work done by computers, businesses saved money and reduced costs. This was passed on to the consumer with lower prices.

On top of this one-two punch, deflation has a productivity gains uppercut that is very strong. This was especially evident in the energy sector. Reducing the cost of fuel exerted a deflationary wave across the board. The ‘shale revolution’ put OPEC on their heels and eventually made the US energy independent. It also steeply reduced the cost of shipping goods to the US and around the world.

This three punch combo was so successful that the Fed was able to print increasingly larger amounts of money, force interest rates down to zero, and not get a significant sustained rise in the CPI.

Above is the year-over-year M2 (blue) and CPI (red). You can see that prior to 1980, the battle was being decisively won by inflation. The money supply was hitting 10% or better and the CPI kept hitting higher highs and higher lows. By 1980 something changed. The red curve of the CPI got knocked to the canvas and never got up.

The Fed hit 10% money growth on several occasions but there was little-to-no reaction by the CPI. Certainly none of the magnitude like the 60s and 70s. It appeared Paul Volcker has knocked inflation out once and for all. The Fed had free reign to print to their hearts content without getting a rise out of their KO’d opponent.

It’s important to know exactly what happened in 1980 to cause such a reaction in the inflation/deflation battle. What Paul Volcker did was break the herd’s mentality that inflation would continue to run higher. He did this in two fashions. First, he froze the printing press. Mr Volcker knew that by printing ever increasing amounts of money, inflation would never be tamed. Take a closer look at the chart above. Chairman Volcker didn’t turn off the printing press, he just didn’t allow it to run hot. By 1983, he did let the money supply have a strong gain but by then, the herd’s mentality was broken.

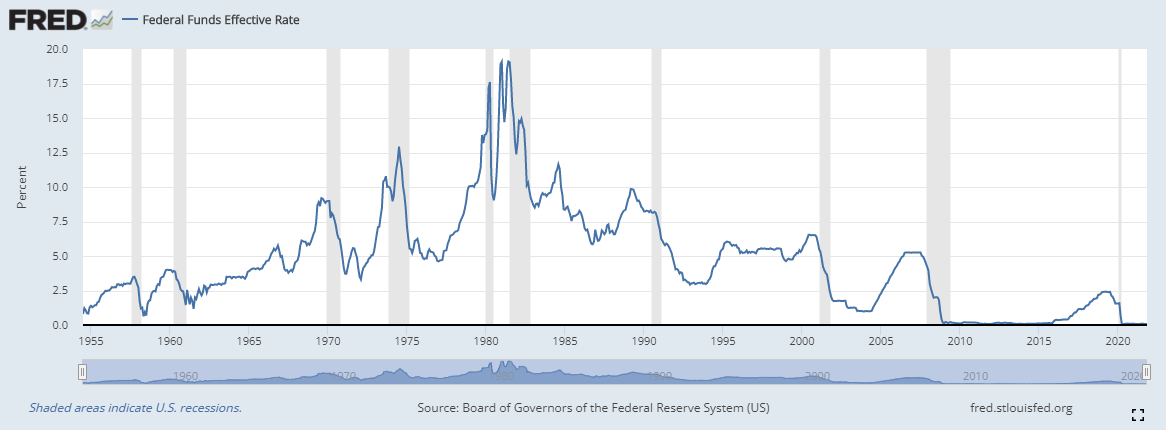

Secondly, Mr Volcker raised the interest rates very high.

The Fed Funds rate hit 19% three times. This signaled the Fed Funds rate high point. Both of these actions had a serious influence over inflation. From that point on the investing world believed that the Fed would take charge if a serious situation arose.

Now to the present. When the economy was shutdown by the government in 2020, the Fed jumped to the rescue. M2 stood at 15.47 trillion dollars in February of 2020. As of October of 2021, it is at 21.19 trillion. That is over a 37% increase in the amount of money in circulation in under 2 years. This is unprecedented in the history of the Fed. This is the direct cause of the recent spike in the CPI. There were direct to taxpayer handouts, bailouts for businesses that were shutdown, and the stock market got a big bailout through the Fed’s asset purchases.

As we’ve seen in the past, deflation’s three-punch combo could knock the CPI back down. What we are seeing however, is a mixed bag. Productivity gains have been constant

or falling.

The shale revolution’s growth has been stunted by the current administration. This has again put the US into a dependent position to help fulfill their energy needs. It has also led to strong oil price gains. The cost to ship goods around the world is beginning to spiral higher. In addition, the port ship logjam is longer than ever. This is inflationary.

Technological advancements continue. Moore’s law is still in effect. It is unknown whether Moore’s law will withstand the test of time. The recent development of AI technologies and the increasing use of internet technologies makes it apparent that this is still a powerful deflationary force.

However, just-in-time-inventory is changing. Businesses got caught flat-footed during the shutdowns. They don’t like telling their customers that there are shortages or back-orders. In time, this could cause a wave of manufacturing to return to the US. In addition, I expect companies to hold higher inventory levels to cushion against future shortages. This will be inflationary.

When this all balances out, it looks like inflation should continue. If it takes hold in the minds of the public and investors, we could see a repeat of the 70s. Some don’t believe that will happen. They point to things like the yield curve or the euro-dollar curve stating that the Fed has made a policy error and a recession is on it’s way.

Recessions are suppose to be deflationary. During a recession, less money is being spent and the demand to hold money increases. There is concern for the future. There is a deleveraging of risk and there are defaults on debt. These are deflationary. This is what others are seeing. This is why the yield curve is doing what it is doing. The hive-mind of the bond market is beginning to believe that the Fed has made a mistake and it is going to lead us straight into a recession.

I believe the same. However, I believe that the Fed will compound this mistake by opening the money floodgates and printing money until the recession goes away. This is exactly what happened in the 60s and 70s. Take a look at a close-up of the M2/CPI graph from earlier.

The CPI may retreat from it’s peak. At this, many will say deflation is back. It will most likely occur during a recession. The Fed will then pump money into the economy. This, in turn, will cause the recession to end but the CPI to shoot up. This happened three times in a decade before the problem was solved. It is a terrible spiral trap. Once the general public believes that inflation will always run higher, the Fed will be trapped. At that point, the only way out will be to channel Paul Volcker. Right now, the Fed is channeling Arthur Burns.

Expect this battle to continue to play out but watch out, inflation has a very sneaky right hook.

I think Volcker the inflation slayer is to buy into a false narrative. He presided over a controlled devaluation of the dollar. The central bank has the option to deflate to the extent that the past periods of over target inflation are corrected. He didn't stop inflation, he reigned it in. He brought the runaway horse to a stop but didn't bring it back to the stable.

His time 79-87 had a cumulative 74% inflation, the dollar lost over 40%. Thats destroying the savers. He made no attempt to disinflate, all was water under the bridge.

If Volcker stands as an example for today, then when a modern Volcker arrives I would be dumping dollars for -anything- else.

I see Volcker as simply managing a controlled devaluation of the dollar (a default basically) and I think thats what the US is doing now. Certainly kudos for not letting the whole thing blow up but I think if you were to ask the now passed on retirees of the period they wouldn't recognise him as an inflation beater.

Thanks Alan! Terrific write up.