Is inflation crashing?

is it time for the Fed to pivot?

The inflation data that has come in over the past two days shows a strong downward trajectory. Yesterday, the CPI was released and it came in under expectations at 5.0%.

While the headline number dropped from 6.0% last month to 5.0% this month, core inflation actually rose from 5.5% to 5.6%.

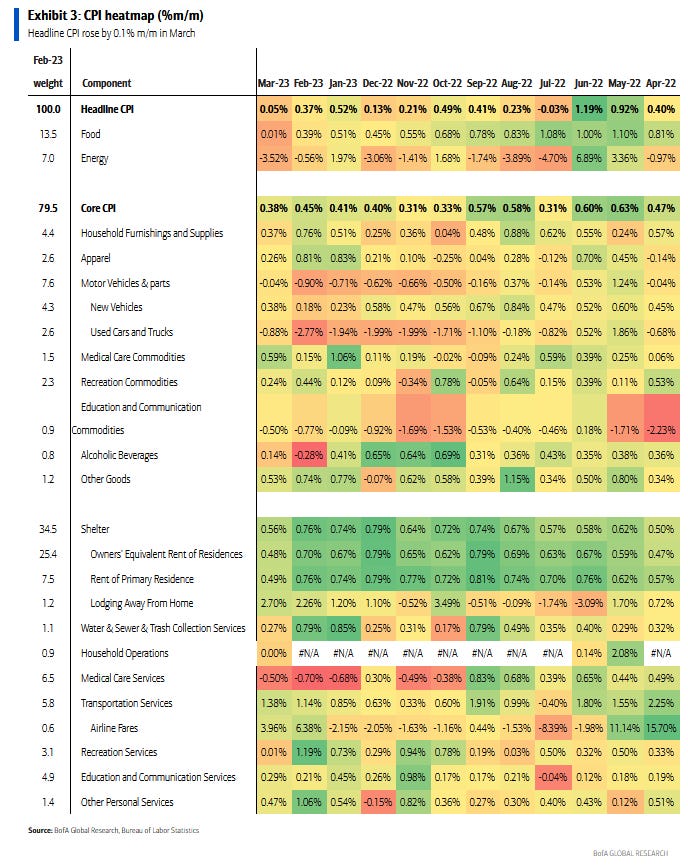

This was largely due to shelter cost increases. Even these costs are beginning to soften. Looking at the month-over-month heatmap, we can see a dramatic cooling effect.

At a 5.0% headline number, inflation is at its lowest point since May of 2021. Looking at the year-over-year heatmap, we can see that the biggest increases this past year have been in; transportation services at 13.88%, food at 8.50%, and shelter at 8.18%.

The biggest decreases were in; used cars at 11.15%, commodities at 10.17%, and energy at 6.42%.

Today saw the PPI data release and it was much the same. The largest components pulling down the PPI were energy related. According to Bloomberg:

Most of the monthly decline in the overall PPI was due to goods, with 80% of that decrease tied to a drop in gasoline.

Seeing the biggest decreases in commodities and energy should make the Fed and Wall street plenty nervous as OPEC+ just cut 1.5M+ barrels per day.

Instead of caution, investors plowed straight ahead raising the QQQ by nearly 2% on the day.

These last two data releases have traders screaming pivot

or at least pause but the CME FedWatch tool still shows a 68% chance of a 25 basis point rate hike coming in May. By July, the FedWatch tool is beginning to price in a pivot and a lower Fed Funds rate.

I believe the last two inflation data releases keep the Fed on track to raise by a quarter point at their May meeting. Even though there has been improvement, inflation is still much too high from the Fed’s perspective. Powell and Williams have continued to pound the table that rates will be held higher for longer and that the Fed’s big concern is loosening monetary conditions too soon and allowing inflation to run hot once more.

My base case remains that the Fed is going to do what Powell has signaled. He wants to get the rate to a level that is sufficiently restrictive and hold it there. I think we are getting close to that “sufficiently restrictive” rate as we’ve seen several poorly managed banks go under. In time I think we’ll also see several over-levered businesses go down. From the latest FOMC meeting notes, we see that even the Fed is predicting a recession later this year.