Leave no deprecated stone unturned

Neo: And why would a program be deleted? Oracle: Maybe it breaks down. Maybe a better program is created to replace it - happens all the time, and when it does, a program can either choose to hide here, or return to The Source.

The Matrix Reloaded

Welcome back to adventures in programming! I’ve been testing out different python libraries and projects in an attempt to find something that would give me historical options pricing. I think I am getting closer but I’ve run into a lot of deprecated dead ends. Deprecation should be a four-letter word.

Back to finance. I built a program to analyze ETF sector performance and used it to analyze sectors for the first 2 years after Trump’s first election win in 2016.

This has a date range of 11-7-2016 to 11-7-2018. The big winners here were:

XLF took an early lead until XLK broke out after March of 2018 evenutally peaking at over 60% gain. I then compared it to the current setup.

Financials again soared immediately after the election. Materials (XLB) peaked on the 11th and now energy (XLE) has taken the lead.

I took this a step further and thought about how reduced regulations really provide an advantage for the smaller companies and that if team Trump is going to be effective in their campaign promise to cut government red-tape, then these smaller companies should see the most benefit. Last time around it looked like this:

This is what we are seeing this time around:

The small cap index, Russell 2000, got off to a hot start in 2016 but was soon caught and surpassed by the tech heavy QQQ. This time around it isn’t much different. The Russell is leading the pack out of the gate.

My curiosity didn’t end there because I’m looking for the absolute best vehicle to express how this dynamic will play out in the market and I think I found it.

Small cap growth (SLYG) could be the biggest winner of the bunch. During the first two years of Trump’s first term, it rocked higher than the QQQs and XLK eventually peaking at over a 60% gain in under two years. Small caps are known for their volatility and this one is no exception.

Here is the performance since Trump’s win on election night 2024;

It shouldn’t be shocking to see small cap value (SLYV) charge higher. There are a few different pieces in play this go around. A big one is the Fed.

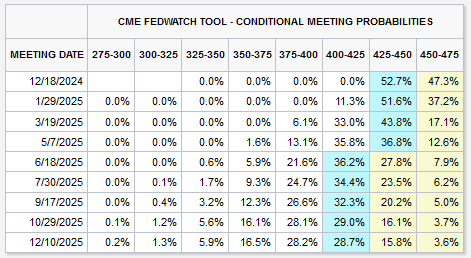

Interest rates are much higher than they were at the start of Trump’s first term. My previous blog looked at the FOMC’s interest rate decision in November.

I asked in that story what “works” Powell and company would need to see in order to know when they’ve hit the neutral rate. This is because I believe we are already at that neutral rate and that the Fed is goosing the market by continuing to cut.

In Edward Chancellor’s “The Price of Time”, Mr Chancellor quoted Walter Bagehot who stated that John Bull can’t stand 2% interest rates. John Bull is the personification of England. Similar in how Uncle Sam is a caricature of America. By stating that John Bull couldn’t stand 2% interest rates, what Bagehot was saying is that the lower bound isn’t 0%, it is 2%. When interest rates are below 2%, John Bull goes mad. You can think of this as irrational exuberance or a reach for yield (buying riskier assets in order to achieve higher yields). Lowering interest rates in this manner distorts the market to an extreme.

The USTreasury yield curve has risen dramatically over the past 8 weeks. We are rapidly moving towards a flat curve which is an improvement over an inverted one. This means that bond holders believe that longer dated bonds should command a premium over shorter dated ones. This is normal. This prices time appropriately. It’ll be interesting to see how the market digests this information. My belief is that we have had a rolling recession for the past two years but now good times are ahead.

The reason there was no official recession announcement from the NBER is pretty obvious. I’m hopefully that the market was able to properly discount how politicized our institutions have become and be able to move forward without panic. If it isn’t obvious that the books have been massaged, you haven’t been paying attention.

Finally, we know good times are ahead because today saw the release of the S&P Global US Composite Purchasing Managers’ Index (PMI) in which Chief Business Economist Chris Williamson stated:

"The business mood has brightened in November, with confidence about the year ahead hitting a two-and-a-half year high. The prospect of lower interest rates and a more pro-business approach from the incoming administration has fueled greater optimism, in turn helping drive output and order book inflows higher in November.

This is exciting but just wait until January when companies begin spending on capital expenditures with the expectation that the Trump administration will create generous depreciation deductions in the tax code.

> The USTreasury yield curve has risen dramatically over the past 8 weeks. We are rapidly moving towards a flat curve which is an improvement over an inverted one.

Doesn't that predict a recession, though? If the yield curve is finally coming out of inversion now, wouldn't we expect to see a recession ~6 months later?