Money Supply and Margin Debt

and a portfolio update

It has now been 46 weeks since the M2 money supply has hit a new high. M2 peaked on April 18th at $22.05 trillion dollars. It has since steadily trended downward.

This has absolutely destroyed my beautiful 13-week annualized money supply chart as well as unprofitable companies, unhedged banks, stable-coins, and other crypto assets such as NFTs.

According to my calculations, the 13-week annualized money supply continued to slow at a rate of -5.43% through March 6th. Here is a breakdown of the past 10 weeks’ worth of data.

As a side-note, my 13-week annualized money supply chart is getting a little busy. Future money supply charts will display fewer years’ worth of data.

The 13-week chart is incredibly awkward at this point. Money supply has been kept flat by the Fed for a long time. This has distorted my chart in ways I didn’t think were possible. There is still money sloshing around in the system from 2020 but it is quickly getting drained out by the Fed’s actions in both the treasury market and the repo market. At some point I would expect a “credit crunch”. This is when banks stop lending. They don’t lend to each other and they don’t lend to consumers or businesses. This would be highly deflationary.

The problem with this scenario is that no progress has been made to develop new sources of raw commodities, including energy. In addition, the actions of de-globalization and de-dollarisation are highly inflationary. These two worlds are colliding, rapidly.

In new de-dollarisation developments, China and Saudi Arabia have developed a deal to build two oil refineries. From MSN.com:

SINGAPORE (Reuters) -Saudi Aramco raised its multi-billion dollar investment in China by finalising and upgrading a planned joint venture in northeast China and acquiring an expanded stake in a privately controlled petrochemical group.

The two deals, announced separately on Sunday and Monday, would see Aramco supplying the two Chinese companies with a combined 690,000 barrels a day of crude oil, bolstering its rank as China's top provider of the commodity.

As the petrodollar slowly dies, the world increasingly moves towards a multi-polar, multi-currency settlement. This should be bullish for commodities but especially gold because gold is money.

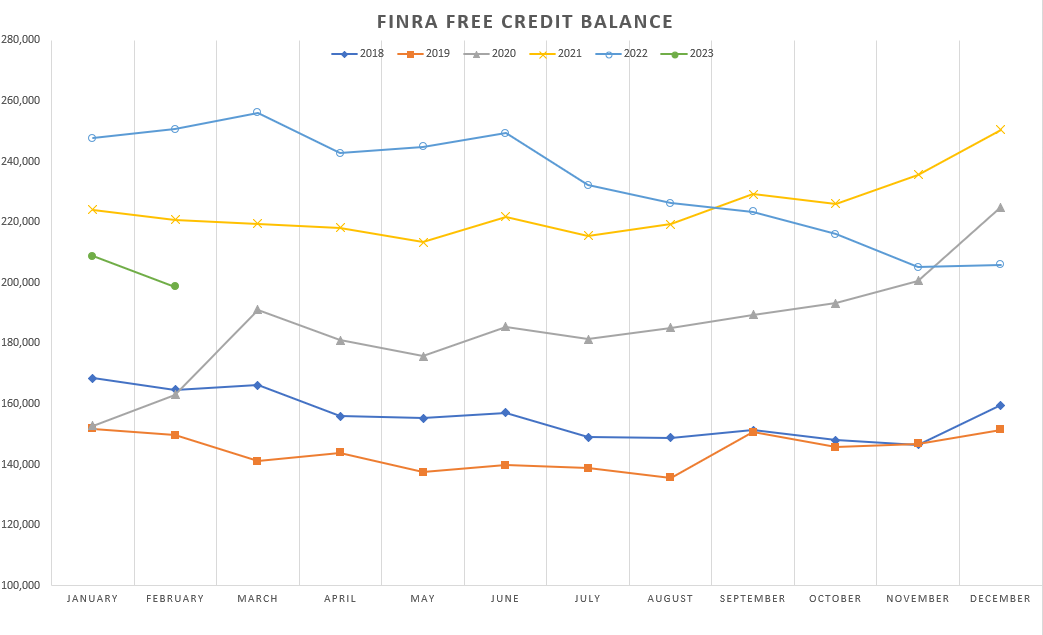

Traders are continuing to pull back on their use of margin. I’m also seeing less “cash on the sidelines” (free credit balance).

My guess is that a lot of money is flowing into short-term CDs, Tbills, and bonds. Powell has made saving great again. As the interest rate has risen, banks are now competing for deposits. There is going to be a transition period here where the banks with superior management teams and balance sheets are going to be offering great opportunities to be a saver with high CD rates and decent savings account interest rates. Personally, I’ve bought a couple but the real news for my portfolio is