Money Supply, Yield Curve, and earnings

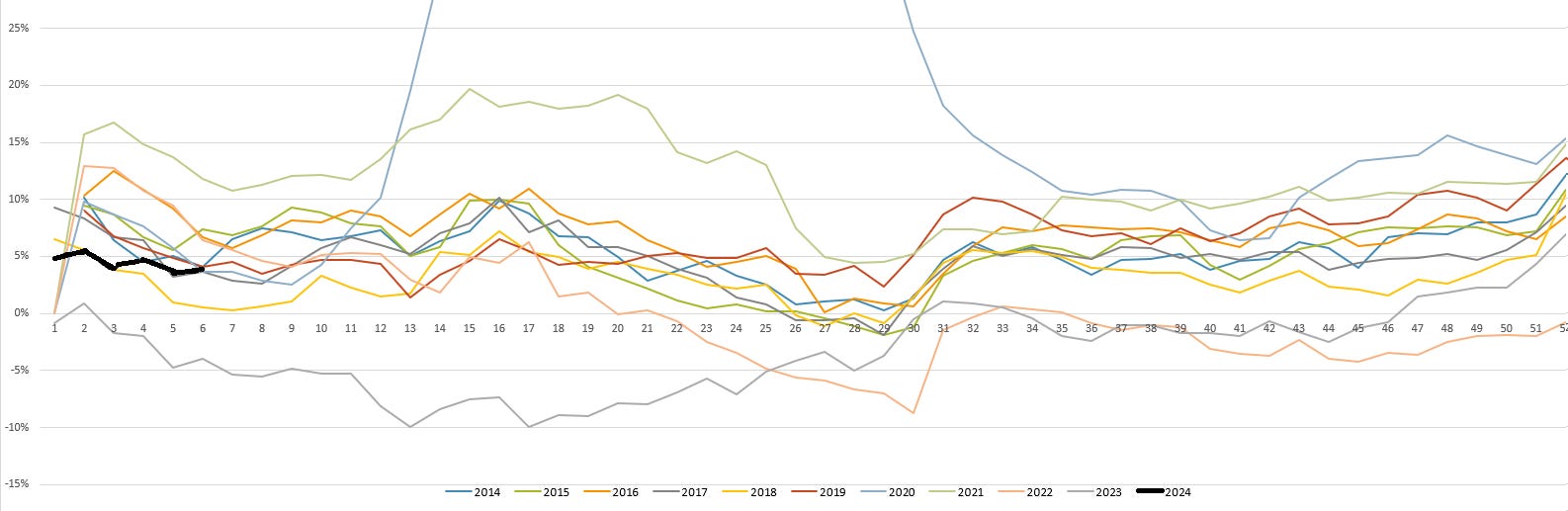

This week the Federal Reserve printed their H.6 Money Stock Measures report. In the past I had run a chart of the quarterly change in the M2 money supply. This was inspired by Robert Wenzel’s work. Here is an updated view on that chart.

After four wild years, M2 is attempting to slide back into the mean trend.

The recent increase in M2 doesn’t show well in the 20 year view but the trend was clear. Thinking about timing (bad idea, I know) it looks like you could add one more October surprise to the list because it appears the former trend could converge with the actual M2 supply by the end of the year.

My preferred measure of inflation (Case-Shiller Home Price Index) came out on Tuesday..

while the Fed’s preferred measure (core PCE) was released on Thursday.

It continues to trend down which the market took as good news as the S&P500 gapped higher and finished the week strong.

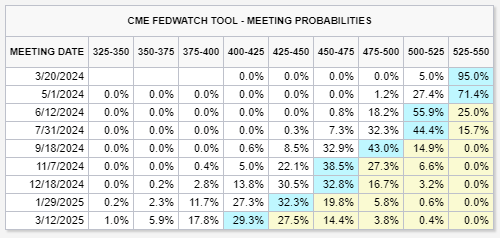

However, the market continues to overestimate rate cuts.

It has started to come to its senses. It is now pricing in three cuts for 2024. This was the Fed’s original outlook from their December 2023 meeting. I continue to doubt that we will get this many interest rate cuts and I think we are starting to see Fed speakers say the same thing. Even CNN Business has even picked up on this.

“I don’t think it’s likely that the committee will reach a level of confidence by the time of the March meeting to identify March as the time to do that,” Fed Chair Jerome Powell said of possible cuts at the Fed’s January meeting.

Now, some economists think the Fed won’t cut interest rates at all this year.

The economy is not slowing down and some underlying measures of inflation are growing, said Torsten Slok, chief economist at Apollo Global Management, in a note to investors Friday.

“The Fed will not cut rates this year and rates are going to stay higher for longer,” he added.

Richmond Federal Reserve President Tom Barkin echoed the idea that the central bank may not cut interest rates this year.

“We’ll see,” Barkin said in an interview with CNBC on Friday morning. “I’m still hopeful inflation is going to come down, and if inflation normalizes then it makes the case for why you want to normalize rates, but to me it starts with inflation.”

This means US Treasuries should retest the highs from last October.

We are in the thick of earnings season. International Seaways posted earnings yesterday and Tidewater announced today.

INSW showed a great increase in year-over-year net income (556.4M vs 387.9M). Last year they returned $320M to shareholders, $308M in dividends. That represented $6.29/share. This year they are increasing the dividend. The first quarter will be $1.32/share which is 2.4% (stock price at $54). If they keep it steady throughout the year, this’ll be a 9.8% dividend yield.

Meanwhile, TDW took off today on the news that they will be buying back shares.

Board approves a new share repurchase authorization of $48.6 million, the maximum permissible amount under existing debt agreements

Tidewater has positioned themselves very well for continued success.

I’m looking forward to GeoPark’s earnings on March 7th. Their latest corporate presentation looked awesome. I especially liked this part:

We’ll see what they have to say Thursday. Finally, Parex had their earnings. I’m still getting to know these guys. It looks like they go ex-dividend March 15th, so that gives me a little to dive in.