PCE and productivity

The Personal Income and Outlays report came out on Friday. It contained the Fed’s supposed favorite inflation metric, the PCE Price index.

Still above 2. The pace of decreasing has slowed. It looks like we could be settling in at a permanent higher plateau. It is possible that this be reignition toward higher inflation. Time will tell.

Yahoo Finance was sure it meant it was near time to pivot.

Thankfully my troubles were eased when they included a picture of my favorite member of the Fed, Governor Waller, in the article.

He had a speech this past week which was well done but not widely distributed.

“I concluded then that we needed time to verify that the progress on inflation we saw in the second half of 2023 would continue, which meant there was no rush to begin cutting interest rates to normalize the stance of monetary policy.”

“Indeed, it tells me that it is prudent to hold this rate at its current restrictive stance perhaps for longer than previously thought to help keep inflation on a sustainable trajectory toward 2 percent.”

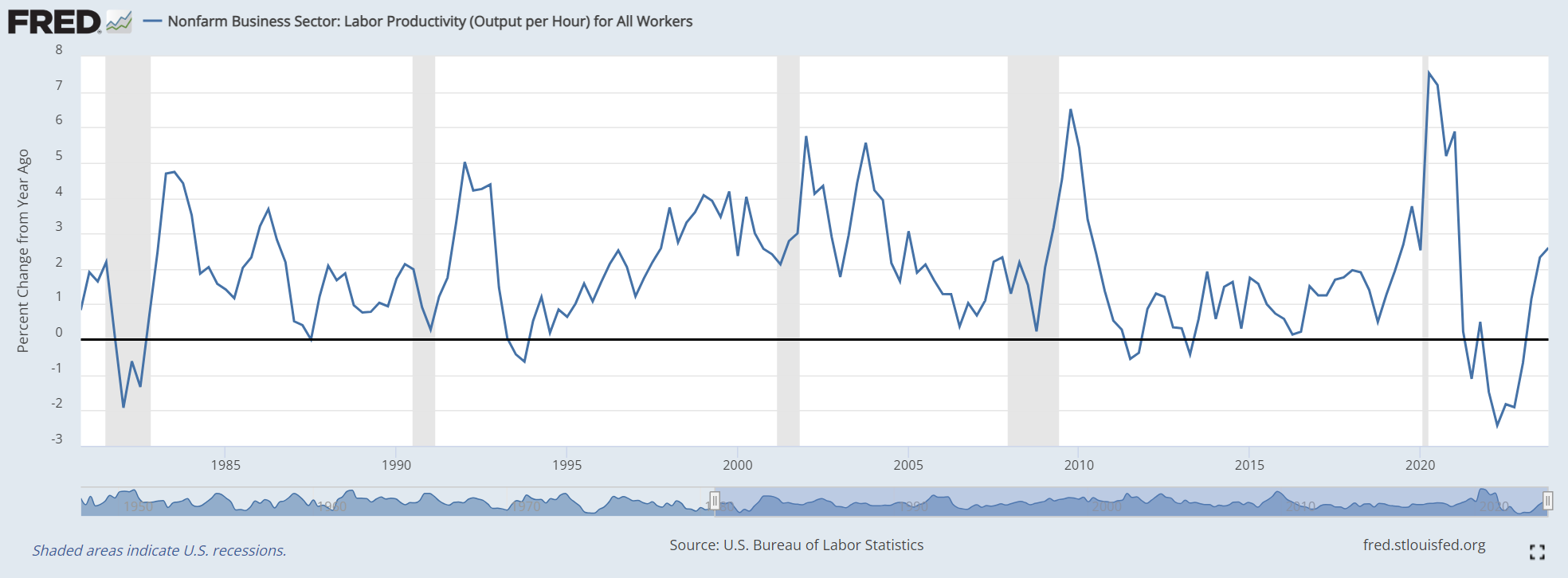

He went on to highlight productivity.

I found productivity graphs on the Fed’s website to be very interesting.

Productivity’s correlation with interest rates and y/y return in capital assets were very interesting. I also noticed that productivity correlated very closely with recessions prior to 1980.

Productivity gains should lead to deflation. A good type of deflation that would translate to a higher standard of living. Goods and services would be offered more efficiently. This would be opposite the kind of deflation that comes from a credit event.

On Friday, Powell traveled to San Fran and sat down for a chat. He added further clarity to his latest post-FOMC press conference.

Some quotes;

“PCE coming in at expectations”

“The fact that the US economy is growing at such solid pace. The fact that the labor market is still very very strong. Gives us the chance to just be a little more confident about inflation coming down before we take the important step of cutting rates. So we are not going to take that step until we are confident.”

Sounds like higher for longer. Maybe the market is going to figure it out. Weird things are appearing in the interest rate prediction market.

And I think we are going to see a retest of the previous highs in the US Treasury bond market.

To those holdouts that still think that the Fed is cutting three times this year, I have only one thing to say: The Fed isn’t cutting three times. Search you feelings. You know it to be true.