Round 2 is coming

Inflation data came out hotter last week than expected. Year-over-year CPI came in at 3.5% above estimates of 3.4%. Core of 3.8% was also up over expectations of 3.7%.

The Producer Price Index was also higher than expectations.

Yahoo made a nice graphic to display where the inflation was at:

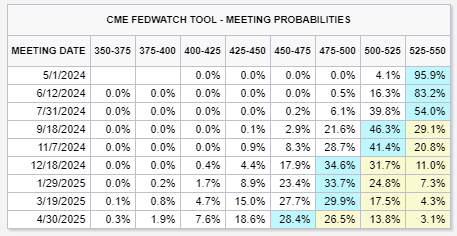

These inflation reports have changed the perception that the Fed is going to cut rates soon. Probabilities have now all moved up aggressively.

In addition, we are beginning to see the foundation being laid for a second round of rate hikes.

“Fed Governor Michelle Bowman, arguably the central bank’s most hawkish voice, recently said that she would favor a rate hike “should progress on inflation stall or even reverse.”

Minneapolis Fed President Neel Kashkari last week floated the possibility of not cutting rates at all this year. He also said rate hikes are “certainly not off the table.” But he said they aren’t likely. Kashkari is not voting on monetary policy decisions this year.”

Michelle Bowman’s speech on Friday the 5th was a big shot across the bow.

“However, we are still not yet at the point where it is appropriate to lower the policy rate, and I continue to see a number of upside risks to inflation.”

She didn’t miss a chance to throw Congress and the Executive branch under the bus.

“Another upside inflation risk I see is from additional fiscal stimulus or a higher spend-out rate from existing and new appropriations.”

And the during the big finally, she let the bomb drop.

“While it is not my baseline outlook, I continue to see the risk that at a future meeting we may need to increase the policy rate further should progress on inflation stall or even reverse.”

Yesterday, Fed Chairman Jerome Powell was at the Wilson Center talking with the Governor of the Bank of Canada, Tiff Macklem.

The entire discussion was an hour in length. I thought the most important lines from Powell were:

“recent data have clearly not given us greater confidence”

“Right now, given the strength of the labor market and progress on inflation so far, it’s appropriate to allow restrictive policy further time to work and let the data and the evolving outlook guide us”

This really spooked the markets. The S&P swung wildly all day. It is now working towards a third consecutive down week.

Meanwhile, the US Treasury Yield curve has been busy.

The pink line is the prior peak from October. Rates at the end of the curve are moving higher towards it.