Soft data and hard facts

what a mess!

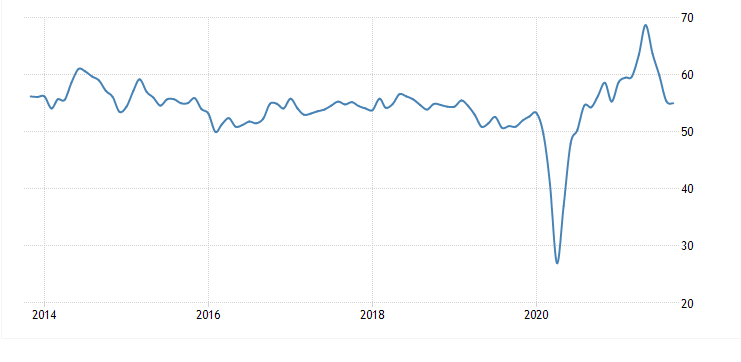

Both Markit and ISM posted their services and non-manufacturing surveys this morning. This is considered “soft” data. This means that they interview business owners and purchasing managers to get a feel for how the economy is going. They then chart the responses and put a number on their survey. A score above 50 means that the economy is expanding, below equals contraction.

Markit’s data came in at 54.9 for services and 55.0 for a composite score. Both indicate the economy is expanding, albeit slowly.

After the rocket higher when the lock-downs eased, the survey data has begun to come back into line with the longer-term picture.

ISM’s goes into a bit more detail in their indexes. They have one for ‘Economic Optimism’ which posted at 46.8. This means consumers are less than thrilled about their current economic situation and are doubtful about improvement. I consider this a sign that consumers are struggling with inflation. They see prices rising all around them and are concerned about making ends meet. This is especially the case for those on fixed incomes like the disabled or elderly. Inflation also puts poor people into extremely difficult situations. Can these people afford rent, electricity, food, and gas this month or is a bill going to have to go unpaid? If so, which one?

ISM also includes in their survey the commodities that are up and down in price.

This continues to be heavily weighted towards increases in prices. The other struggle that these businesses are seeing is employment. It continues to be a major hurdle for them and comes with another price increase. ISM’s employment figure for September came in at 53.0, which is barely expansionary. This tells me that those that were on the unemployment dole have still not gotten the motivation to find work. It could also mean that the boomers that were on unemployment for the past year aren’t coming back to find jobs. We’ll have a better understanding of what we are dealing with when the employment situation report comes out on Friday.

ISM also posts some of the responses that they get to their survey. It is typically mildly entertaining to read through a few of them. This week proved no different.

“Transportation bottlenecks are increasing, resulting in longer lead times and missed appointments.”

“Constraints on logistics from a cost and availability standpoint continue to be an issue.”

“The semiconductor (shortage is) impacting server delivery. Alternate parts and engineering efforts are being used to create workaround solutions.”

“Both domestic and international logistics are increasing lead times about six weeks for ocean freight and two weeks for domestic freight.”

“Inventories shrinking due to global shipping logistics being a seller’s/provider’s market, with primary focus on yield versus market expansion.”

“Still experiencing very strong demand. Supply chain is still a challenge.”

“Demand far outweighs supply for goods and services.”

“We continue to deal with extended delivery lead times and high costs. Stress on the supply chain beginning to be reflected in the quality of products offered and delivered. Current buying strategy is to wait — except with equipment, as (price) increases are expected.”

These are the cold hard facts. Businesses are seeing struggles with logistics while “demand far outweighs supply”. It is interesting to see some businesses looking for “workaround solutions” to their supply issues. It makes me wonder if we could see manufacturing come back to the US. All roads point to higher inflation for a longer time period. The transitory story is falling apart. Even the Fed and government economic advisers are trying to get in front of the story and prepare the masses for higher inflation. The tsunami of inflation is crashing all around. We are seeing oil and natural gas leap higher. Coal, aluminum, and uranium have all pushed higher as well. In time, silver and gold will get their turn. I’m also starting to see opportunities to short interest rates. Have some dry powder ready to go. You never know when silver or gold might catch a bid.