That was a bold move Powell

Let's see if it pays off

I mentioned Wednesday that the FOMC’s 25bp decision was disappointing. Part of this is because it made me re-evaluate my Fed vs ECB thesis. Some questions I had floating around in my head were:

Had Powell never really been concerned with what was going on in Europe?

Is he not attempting to exert control over the offshore dollar market?

Did the NY Banks not really run the Fed?

Does the FOMC not see the data that I’m seeing?

Was there something else in play here?

Did JPMorgan/Goldman-Sachs/Fed want to watch the knife twist more slowly?

Since the make-up of the FOMC has shifted, did Powell lose some of his grip on the power he had at the Fed?

Was Powell more concerned about having a unanimous decision coming out of the FOMC meeting?

Then today happened.

“The unemployment rate in the US inched lower to 3.4 percent in January 2023, the lowest level since May 1969 and below market expectations of 3.6 percent, as the number of unemployed people declined by 28 thousand to 5.69 million and the number of employed increased by 894 thousand to 160.1 million. The latest jobs report came on the heels of a sharp decline in weekly jobless claims to nine-month lows and a larger-than-expected increase in the level of job openings in December to a five-month high, pointing to a still-tight labor market.”

Wednesday’s disappointment now looks like an error on the Fed’s part.

“Total nonfarm payroll employment rose by 517,000 in January, and the unemployment rate changed little at 3.4 percent, the U.S. Bureau of Labor Statistics reported today. Job growth was widespread, led by gains in leisure and hospitality, professional and business services, and health care.”

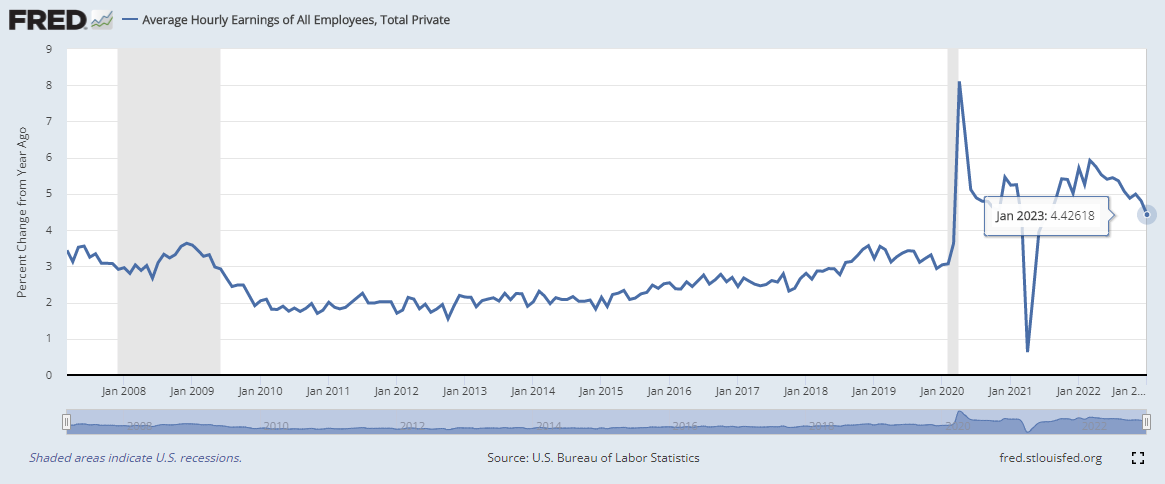

In addition to the total payroll beat, average hourly earnings continues to increase as well as the average weekly hours.

While the average hourly earnings have cooled somewhat, they are still well above the past trend-line (around 3%). A 4.4% year-over-year clip is still a brisk pace.

In addition to the payroll numbers, the ISM non-manufacturing data also makes Powell’s quarter point move look like a policy error.

The headline figure (ISM Non-Manufacturing PMI) dipped below 50 and has quickly rebounded.

There is going to be a lot of data that comes out between now and the next FOMC meeting. Only then will we be able to look back and determine if this 25 point move was appropriate.

Looking at the bigger picture here, while this 25bp move may look like a mistake today, the Fed is still well ahead of the ECB. The more important development that should concern the Fed is the rapid de-dollarization that it happening. The Saudi’s are now open to selling oil in other currencies, BRICS countries continue to work towards a reserve currency, South American countries are working on launching a joint currency, and a new trade corridor between Russia, India, and Iran is working to integrate their banking systems to bypass SWIFT. Better get back to work Mr Powell. You’ve got a lot more to do.

Alan,

Are you saying the rate hike looks like an error because they should've raised a half point? Can you clarify why you think JPOW made a mistake?

"The Saudi’s are now open to selling oil in other currencies"

Cue the next regime change operation....