Happy [belated] Fed Day. Yesterday the Fed announced a 25 basis point increase in the Fed Funds Rate. It was entirely predicted by the CME’s FedWatch Tool,by the FOMC’s prior meeting’s economic projection materials (and they predict another quarter point by the end of the year), and by Mr. Market.

The post-meeting press conference had a few interesting quotes. First up was Powell’s Freudian slip when he began talking about the ECI report. This report comes out of the BLS and Powell called it the “employment compensation index”, when it is actually called the employment cost index. This slip makes me think that the Fed is focusing on employee compensation. We’ve seen several strikes where higher wages were secured, the latest being UPS. Higher wage rates can easily lead to higher inflation. Higher wage rates put more money in the pockets of consumers. Powell expressed that he largely expects a softening of the labor market. I think what we've seen is a softening of the white-collar tech/coding industry while the blue-collar/hospitality jobs are still in high demand.

There were several cleverly worded questions about a pivot or what it would take for the FOMC to cut rates. Powell was firm and stated that “What our eyes are telling us is that policy has not been restrictive enough, long enough, to have it’s full desired effects”. He added later on that “We would be comfortable cutting rates when we are comfortable cutting rates and that won't be this year, I don't think.”

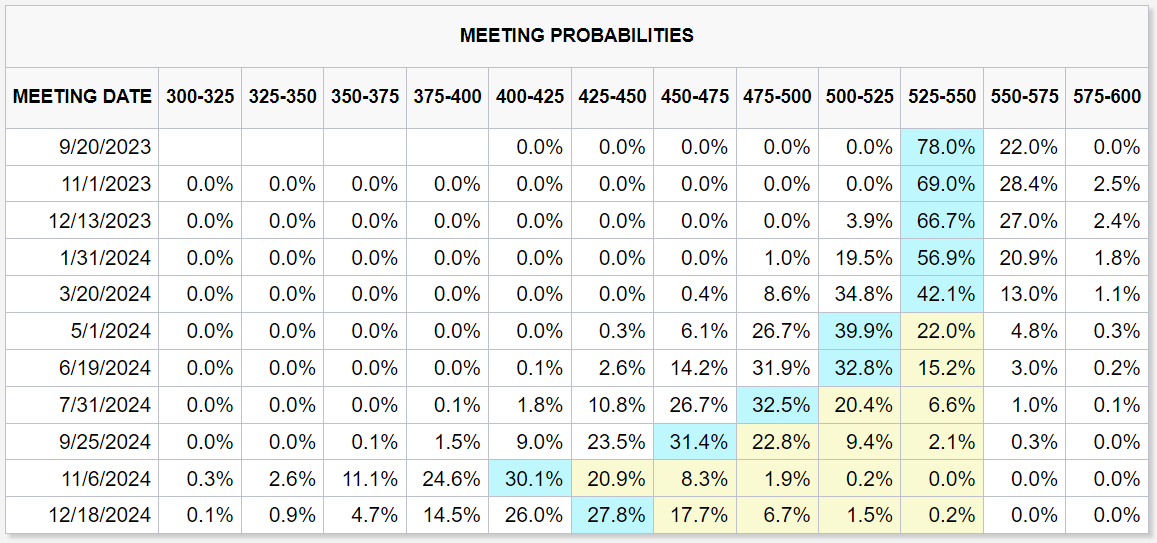

The CME FedWatch tool agrees.

The first rate cut is predicted to occur in May of next year, with rates largely settling in to the 4-4.75% area. To me this looks like current conditions have been projected out further than they should have been. I feel it becomes wishful thinking once you get past the end of 2023. I am expecting inflation to get a second wind towards the end of this year on the back of higher commodity prices, but especially oil. Before that happens, inflation will go lower. My favorite inflation indicator is already showing negative inflation.

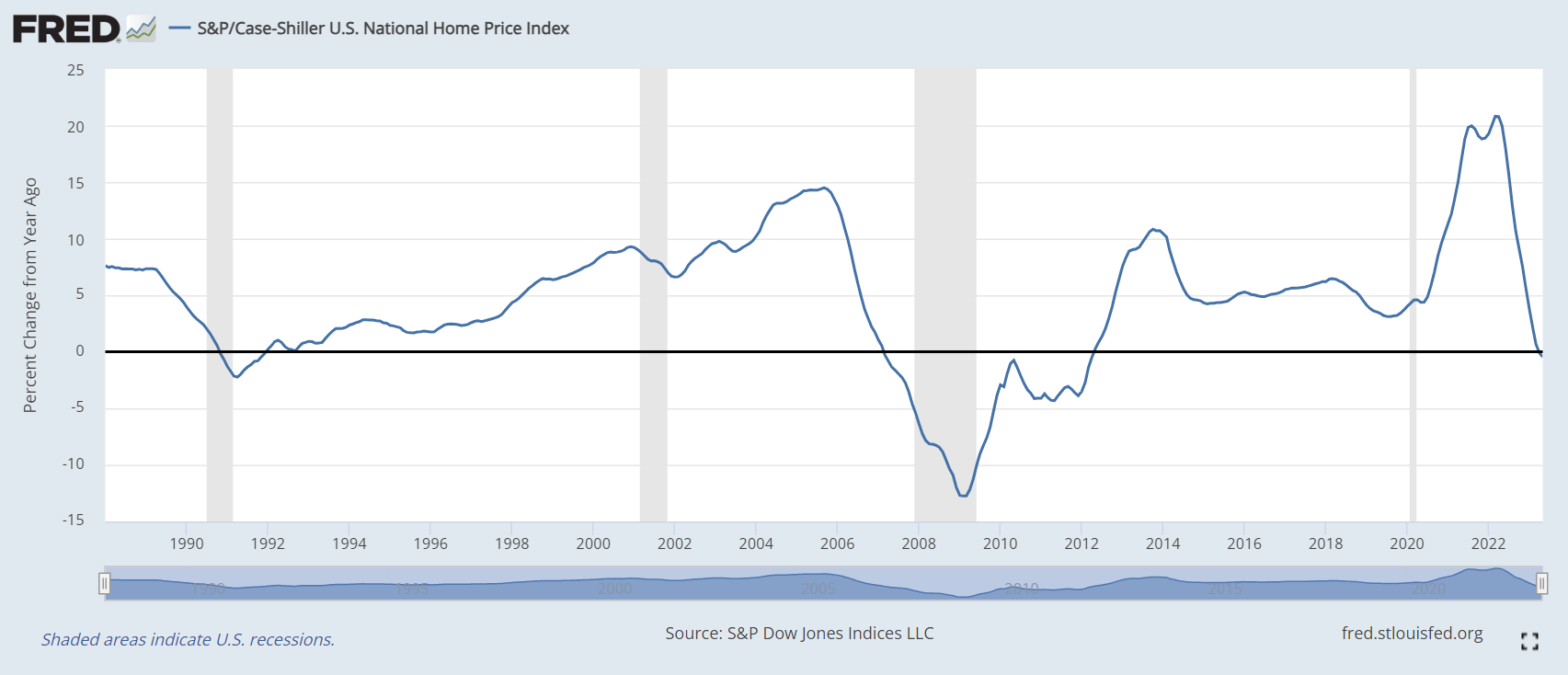

The Case-Shiller home price index has gone into the negative as of May. The housing industry is in a very unique spot. We have tight housing conditions which has boosted the stock prices of many home builders and at the same time, we’ve got really high mortgage loan rates reducing the amount of homes that are being purchased. Those that have to move are moving but those who have locked in a mortgage below 5% aren’t interested in moving and giving that low rate up. In fact, 61% of homeowners have a rate that is under 4%. This dynamic will heavily influence the housing sector moving forward.

Meanwhile, the 13-week annualized M2 money supply report is beginning to get back to 0.

In the past, this kind of prolonged negative money supply growth would have precipitated in a serious credit-crunch, recession, and stock market crash. This creep back to 0 is entirely due to baseline effects.

The most interesting debate to me right now has to do with the yield curve. Will short term rates come down or will long term rates come up.

I think we are starting to see the long end rise. There is currently a lot of pressure on the 10y. This year has seen it rise to 4%. The yield curve will normalize, this I have no doubt. What the curve looks like when it does normalize is an unknown. I largely blame the past 3 treasury secretaries for not extending duration in their bond issuance but Janet Yellen is taking it to the extreme. As an academic she plays largely in theory and not in practice.

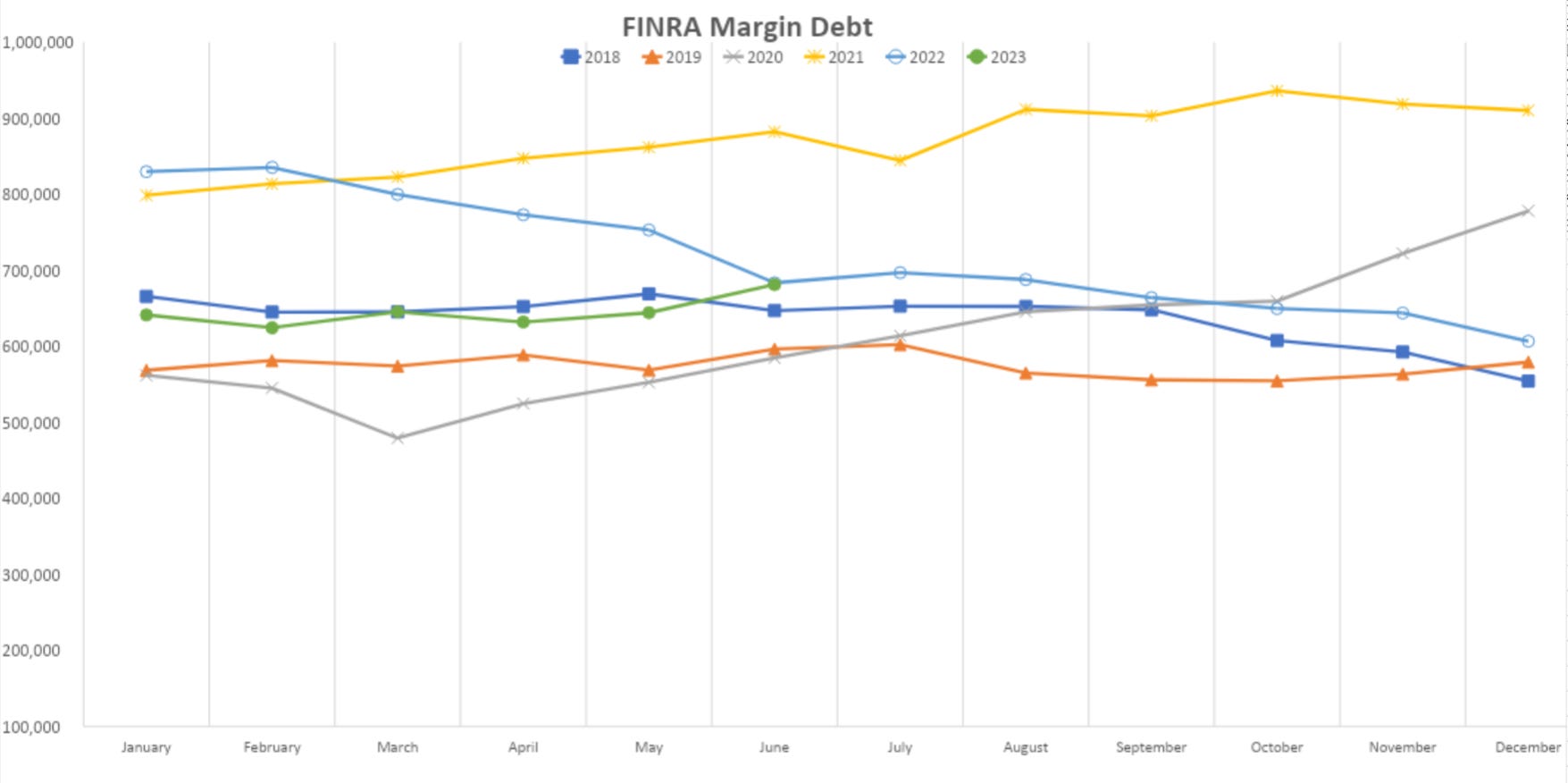

I believe she purposely inverted the yield curve with her own version of operation twist because in theory an inverted yield curve would indicate a recession and caused the Fed to pivot. However in practice, we have seen tremendous Q2 GDP growth, and US consumer confidence hitting two-year highs. Even traders are dipping their toes in the water with a boost in margin debt use.

It feels like many prognosticators are pulling back off the “recession-is-imminent” cliff. It feels like this has been a “rolling” recession. Certain sectors of the economy have been hit, while others continue to trend along. It now feels like we are having a “rolling” recovery. Those sectors that were hit are beginning to get their legs under them again. I find it humorous that this was suppose to be the most widely anticipated recession ever. When everyone thinks alike and has the same prognostication, everyone is likely wrong. Mr. Market has a history of not going along with the crowd.

Could this be the time that the most accurate recession indicator (the yield curve inversion) is wrong? Could this be the time that the best predictor of broad market growth (the M2 money supply) is wrong? Could this be the time that the Fed actually achieves a soft-landing?

While the dollar index might say otherwise right now, I think in short time, the US will once again find itself to be the cleanest shirt in the laundry pile. Economies overseas look much more unsteady. The Fed’s tight monetary policy and use of SOFR has brought home many offshore dollars. This trend is not over yet and the next thing to break could be elsewhere.