The Fed is playing with fire

and it could end up with everyone getting burned.

The US Bureau of Labor Statistics posted the Producer Price Index (PPI) this morning for the month of July. The PPI is the counterpart to the Consumer Price Index (CPI), it is a measure of the prices producers pay.

For all commodities, the index is up 1.2% month-over-month. You can see from the chart below that prior to the government shutdown, the PPI for all commodities would hover between 0% and 1%. It would occasionally get above 1% or go negative. We have now had 15 consecutive months of the PPI being 0.5% or higher on a month-over-month basis.

This has translated into a year-over-year PPI for all commodities of 19.8%! Even at the height of the 2008 saga, the PPI wasn’t this high. For a comparison, I had to go all the way back to…. December of 1974!

This isn’t the first time I’ve made comparisons to the 1970s. These kind of reports really make me anxious to get back into SOG (silver, oil, gold) and the associated miners and drillers. Something to keep in mind is the podcast that I highlighted last week from NPR’s archives titled “The Great Inflation Classic”. In the same way that Paul Volcker broke the herd’s mentality when it came to inflation expectations, the herd’s mentality will break the other way concerning inflation. Once this happens, we will be in for a wild ride.

Employment figures continue to improve. The latest data from the Unemployment Insurance Weekly Claims Report shows that initial claims and continued claims continue their trend lower. I’ve highlighted both of the non-seasonally adjusted (NSA) figures in the small red boxes. I’ve also highlighted the pandemic relief. We had almost 730k people removed from the pandemic assistance dole.

What is amazing to me is the bottom number. We have over 8.6 million people still on the pandemic relief, and as we learned on Monday, we have 10 million job openings. This is going to create a bidding war among businesses for workers putting upward pressure on wages. Money will be burning holes in the pockets of consumers pushing prices higher.

Yesterday I touched on the idea of alternative ways to play the push higher in food prices. I got a reader question on this topic.

How will these stocks do in an environment where supply costs go faster than they can raise prices? I don’t understand this sector well enough to know.

My argument would be that these companies (Tyson Foods, Hormel Foods, and Conagra) employ chief financial officers who wouldn’t be worth their salt if they couldn’t predict what their company needed to charge to remain in business. I understand that prices could get out of hand in a hurry if the herd changes directions. Companies will always be prepared for the future. That is what good businessmen and entrepreneurs are skilled at. The key is finding out which companies they work for.

I initially listed these three because they were at the forefront of my mind. I’ve not done much research on them but so far, Tyson (TSN) looks the best.

For those interested in the fundamentals, I would direct you over to Tyson Food’s page at gurufocus.

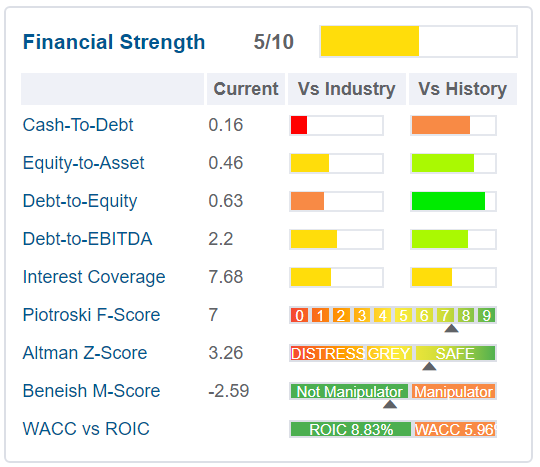

Tyson is highly leveraged right now at 0.16 cash-to-debt. This means they have 16% of their total outstanding debt in cash on their balance sheet. If inflation continues to heat up, Tyson’s debt would become less of a drag on their balance sheet as they would be paying it back with dollars that have reduced purchasing power. The other thing that sticks out to me is that their weighted average cost of capital (WACC) is less than their return on invested capital (ROIC) by 2.87%. This means that the money they have borrowed has been put to good use.

On the profitability side, their operating margin is one of the best in their company’s history. Also, their return on equity (ROE) and return on assets (ROA) both look strong. Return on equity would be the company’s net income divided by the balance sheet equity (assets minus the liabilities). The ROA would be simply the net income divided by the assets listed on the balance sheet.

In addition to their strong position they pay a dividend with a yield of 2.24%.

Since they recently had their earnings call, the press has jumped at their revenue forecasts with pieces like this: https://www.reuters.com/business/retail-consumer/tyson-foods-raises-2021-revenue-forecast-strong-beef-demand-2021-08-09/.

Unfortunately, Tyson is also in the news today because some of their workers are protesting the company’s decision to mandate the jab.

These kinds of wild card factors are hard to take into account when analyzing companies versus a pure play in the underlying commodity. My advice is, do your due diligence on these companies. Gurufocus’s website is a good start, but actually looking at the data on the SEC-Edgar website is best. They could turn out to be big winners but if too many non-fundamental factors exert influence on them, they could lead to nowhere or worse, a loss of capital.