This week's round-up

and what I'm doing this weekend

Tuesday saw Fed Chairman Jerome Powell sit down with David Rubenstein at the Economic Club in DC. I watched it live. You can see a replay of it here (Bloomberg Youtube). I also found this pdf which had a decent transcript of the event. There was little in the way of new revelations (outside of Powell’s salary and guitar playing). The dis-inflationary process has begun. The Fed is attempting to achieve a policy stance that is restrictive enough to bring inflation down to 2%. They believe further rate increases will be appropriate and they plan to hold rates higher for longer.

Rubenstein attempted to lead Powell on a few questions. Specifically if he gets an early preview to certain data releases (he does) but there was no real follow-up. Did Powell know the Friday jobs number was going to be a blowout? I think this is a distinct possibility. Makes me think that the 25bp increase in the FFR was intentional in that he gave the market exactly what it wanted, good and hard.

One last thought on the interview, the dis-inflation process that Powell has talked about is being seen in the goods sector. This is tied directly to commodity costs. Many commentators (including the Fed) have tried to analyze (or control) demand but the real story is in the supply side of the equation. There has been very little in the way of new streams/sources of commodities. With supply continuing to dwindle, prices for base commodities will continue to stay high and may easily go higher.

A secondary inflationary wave is coming if there is not significant money spent on capital expenditure in the goods sector. This makes rising interest rates a two-edged blade. While higher rates cut down the unprofitable tech, excessive market speculation, and restricts demand it also restricts investment in new developments. New commodity projects will need to return in excess of financing costs. This will be true in all things. In addition, if you can get 5-7% on T-bills, why would you put your money to work in the housing sector, the S&P500, new oil wells, new copper mines, etc. if those things won’t return something more than 5-7%?

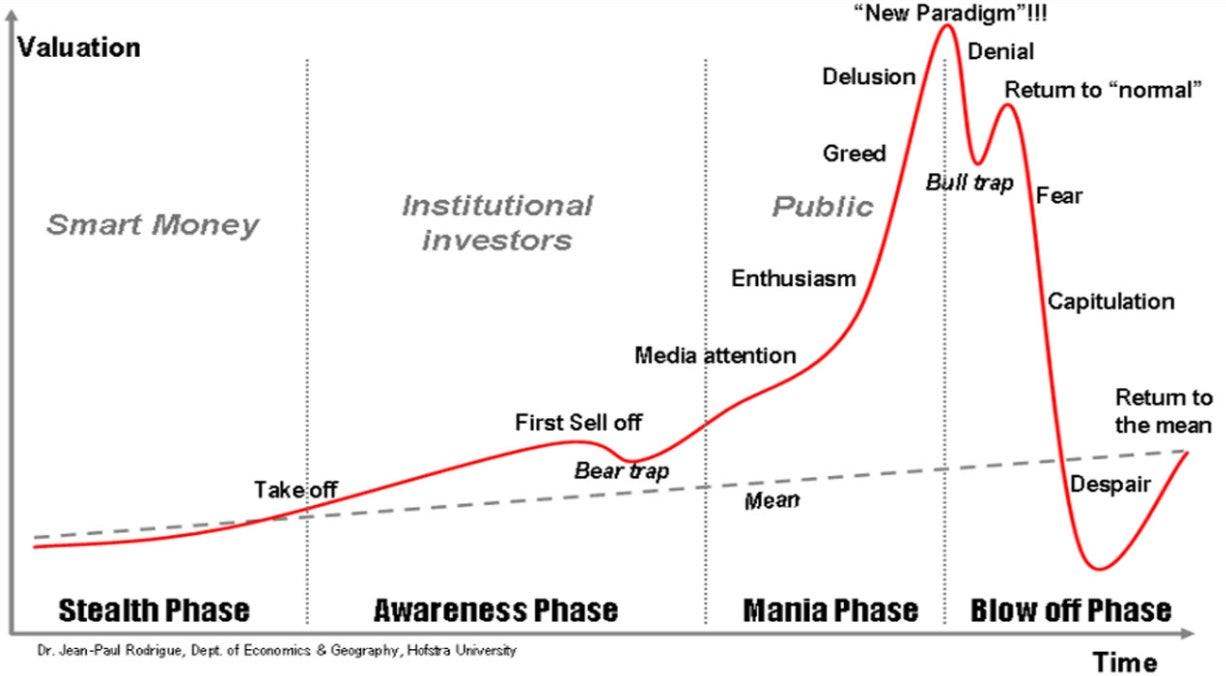

The timing on this is going to be tricky. There is going to be a period of time that things are going to look “normal”. The markets will have adjusted to higher interest rates and things will look like they are back on track. I feel that January is an excellent example of this. It had all the makings of a “bull trap”/“return to normal” scenario.

Yesterday JPMorgan’s CEO, Jamie Dimon, sat down with Reuters for an interview.

The chief executive of JPMorgan Chase & Co., the biggest U.S. bank, cautioned against declaring victory against inflation too early, warning the Federal Reserve could raise interest rates above the 5% mark if higher prices ended up "sticky."

Jamie Dimon's warning came after Federal Reserve officials said more rate rises are on the cards, although none were ready to suggest that January's hot jobs report could push them back to a more aggressive monetary policy stance.

In reference to inflation, Dimon said "people should take a deep breath on this one before they declare victory because a month’s number looked good."

"It’s perfectly reasonable for the Fed to go to 5% and wait a while," Dimon said.

The idea that interest rates are going to be higher for longer is only now beginning to sink into the hive mind of the market.

This interview with Dimon really sets the stage for next week when the CPI will be released Tuesday.

I fully expect a surprise lower on Tuesday. This would really tie in well with Dimon’s idea that we shouldn’t “declare victory because a month’s number looked good”. The market was slow to anticipate the increase on the way up and now they are going to be slow to anticipate how fast inflation is going to drop. At some point, there is going to be a pivot but it won’t come from the Fed. It’ll come from higher inflation prints because no new streams of goods are coming online. Like I said above, the timing is going to be very tricky. In addition to the CPI, the PPI comes out on Thursday.

If you want to follow along with what I’m reading/listening to this weekend, this is what I have on tap:

Seymour Hersh’s Nord Stream article

Tom Luongo’s podcast #130 with Alex Krainer

ValueHive’s podcast with Shrubbery Capital Part 2

(and because March Madness starts early in my household)

Duke v Virginia, Temple v Memphis, Clemson v UNC, UCLA v Oregon, UConn v Creighton