To recess or not recess, that is the question

"Labor was the first price, the original purchase-money that was paid for all things. It was not by gold or by silver, but by labor, that all wealth of the world was originally purchased."

- Adam Smith

All the important labor reports were released last week.

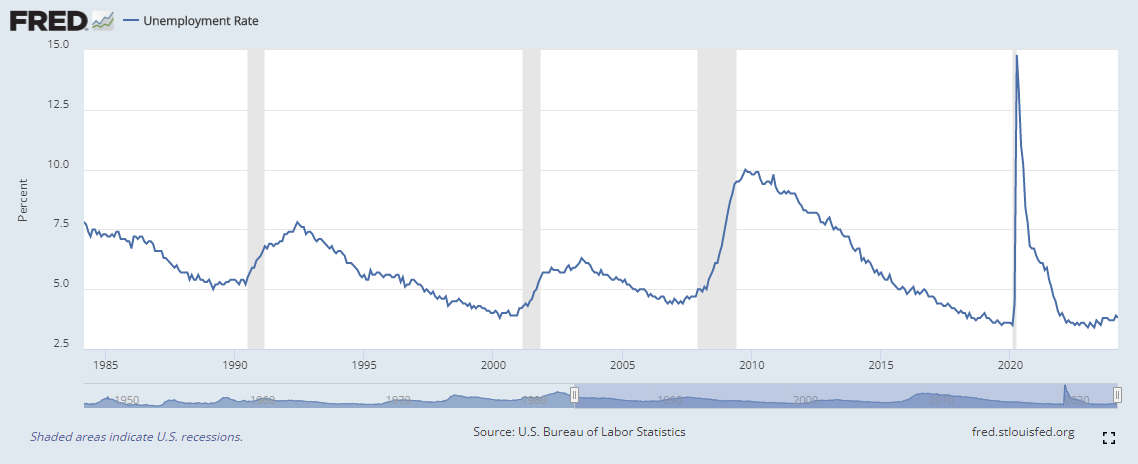

The US unemployment rate came in at 3.8%. It continues to stay in a tight range. The number of unemployed individuals decreased by 29,000 to 6.4 million. When combined with the JOLTs report, we can see that the labor market is starting to come back into a better balance.

After an amazing run, the job openings divided by the unemployment level is showing that there are still 1.36 jobs per unemployed person.

TradingEconomics tells us where the jobs are at:

“The number of job openings went up by 8,000 from the previous month to 8.756 million in February 2024, above market expectations of 8.75 million. During the month, job openings increased in finance and insurance (+126,000); state and local government, excluding education (+91,000); and arts, entertainment, and recreation (+51,000). On the other hand, job openings decreased in information (-85,000) and in federal government (-21,000). Regarding regional distribution, job openings fell in the Northeast (-2,000), the South (-62,000), and the Midwest (-9,000), but rose in the West (+81,000).”

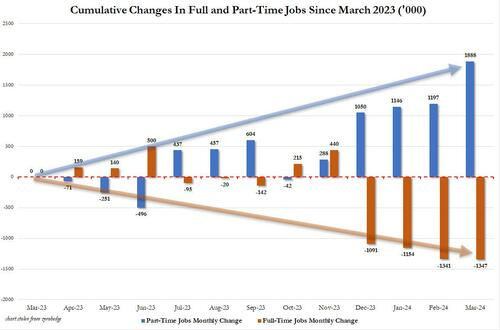

I saw many takes on how the part-time employment is far exceeding the full-time employment. Hence the lead meme. Zerohedge’s article comes to the front of my mind but they were far from the only one. Here is a graphic from that article:

I think this is the wrong thing to focus on. When you see the full picture, a different story takes shape:

For me, focusing on part-time jobs or part-time versus full-time is a fools errand. Part-time jobs could be plentiful for many reasons that don’t have to do with a recession. The problem for me is that when full-time employment rolls over, we typically have rough waters ahead.

Look how nicely all those shaded recessions line-up with negative full-time employment growth. Uncanny. This seems to be another indicator with a long track record (like the yield curve inversion) that shows us a recession should be happening. Yet, economic growth in the US seems to power ahead.

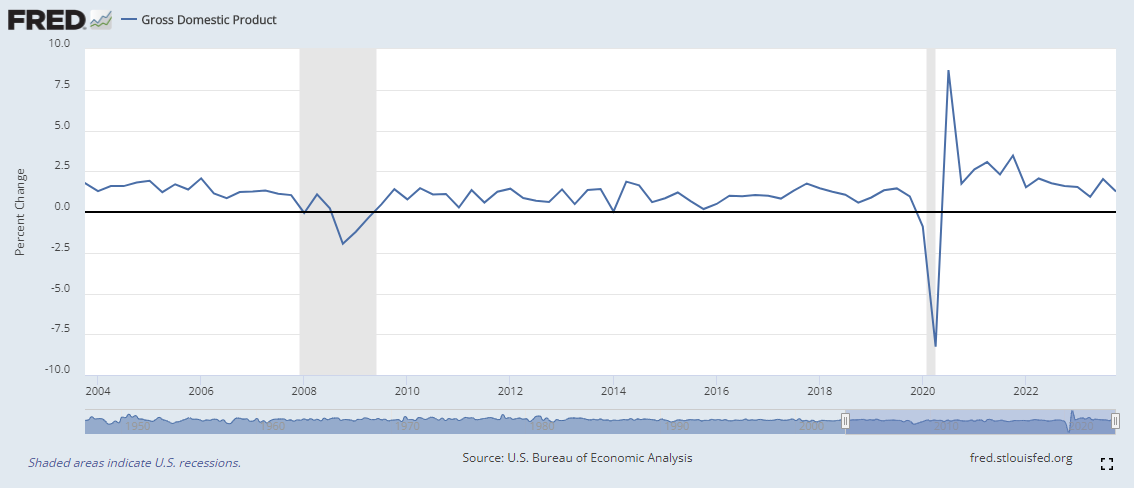

The Atlanta Fed’s project, GDPNow, is showing growth in the 1st Q at 2.8%.

This gets back to the fundamental change that has happened in monetary policy. Nearly two years ago I wrote about how the LIBOR rate was getting replaced by the SOFR rate. This changed the way the bond market worked in the United States. No longer was the Federal Reserve dependant upon 17 foreign banks to determine what rate Americans should be lending money to each other. This break in policy shook central banks out of the “coordinated monetary policy era” and set Powell on the path to a 5.5% Fed Funds Rate. With the Fed off the lower-bound, we are beginning to see the effects of higher interest rates. It is exposing the mal-investment in the economy. As this mal-investment gets liquidated and zombie firms go bankrupt, those resources are then sold to entreprenuers who are able to utilize those resources more efficiently. This makes the economy more productive. At the same time, it appears to be gearing up for war. Gold is up, Bond yields are up, and oil is up. The next “up” could be inflation.