Unemployment and new rules to trade by

for Fed members

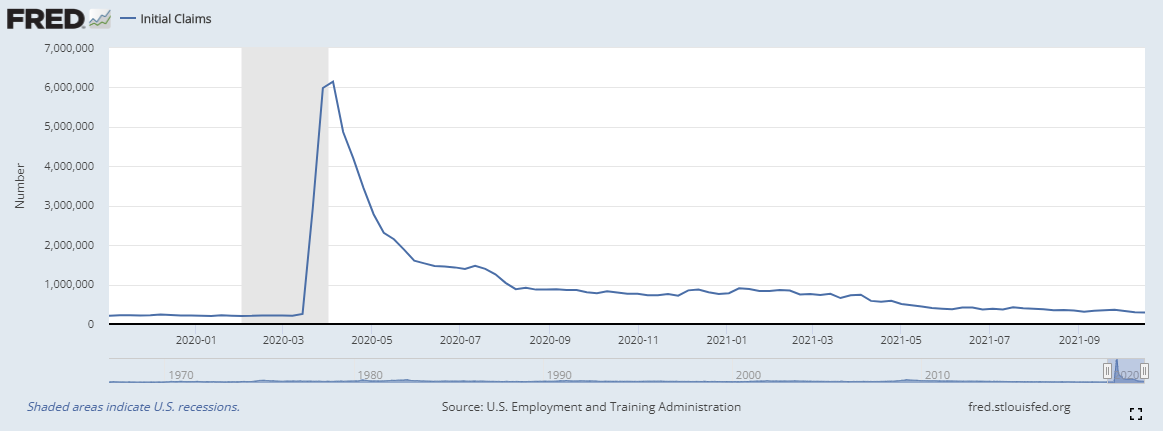

Weekly unemployment figures were released this morning. We are continuing to see a return to normal. The total number of unemployed has dropped to less than 3.3 million.

Initial claims are swiftly moving into the range they were in prior to the government shutdowns.

Continued claims also has begun to push back into a “normal” range.

This sets the stage for the Fed to kick-off the taper at their next meeting, which is a little less than 2 weeks from today. It was also a reminder to traders that the taper is coming. Today saw an initial drop across the spectrum as traders braced for the taper. SPY, oil, gold, silver were all lower right out of the gate. All steadily climbed towards the end of the day’s trading session.

While unemployment is getting back to “normal” levels, one thing that is not is volatility. Both bond market and stock market volatility have continued to remain elevated since the government attempted to shutdown the economy. Both of these indexes are measured by the Chicago Board Options Exchange (CBOE). First up is the VIX which measures near term volatility which is expressed by stock index option prices.

Also, I have the CBOE’s 20+ year treasury bond ETF volatility index as a gauge of the bond market’s volatility. Again it shows similar elevated volatility prior to March 2020. The bond market volatility is much more subdued vs the VIX. This is because bonds don’t trade at the same frequency that stocks and options do. The VIX is much more sensitive to market dynamics. Still, this looks concerning if you are a bond trader.

Increased volatility translates into wider bid-ask spreads and bigger swings in prices. It means traders are becoming less sure of the future. The stock market and bond market discount the future back to the present. This means that traders attempt to predict the future and then try to lower their expectations. In the industry there is a formula to follow. It is the discounted cash flow (DCF) model. Current company cash flows are predicted out 20-50 years and then reduced back to the present to try to guess at what the company should be worth. This model relies heavily upon low interest rates to make those future cash flows look large. Higher interest rates would weight on this model and increase the discount of those future cash flows.

The mega budget-busting bills that are being debated in Congress, the shortages and logistical issues facing companies, and the Fed’s taper all add to the cloudiness of future predictions.

The Fed is finally attempting to put a stop to the allegations of insider trading. They’ve announced new rules for Fed Presidents and Governors to trade the stock market. Jerome Powell assured the public that,

"These tough new rules raise the bar high in order to assure the public we serve that all of our senior officials maintain a single-minded focus on the public mission of the Federal Reserve.”

All I can say is better late than never, Jay. If you would have put out this kind of statement in the beginning, you might have been able to avoid the embarrassment of your poor trading and the insider trading of your fellow Fed members.

The new rules restrict Fed members from purchasing individual stocks. They are now only allowed to own broad-based products such as market indexes, ETFs, and mutual funds. They are also required to provide 45 days’ advance notice for any purchases or sales of investment vehicles. Finally, they will be required to hold any investments for a minimum of one year.

These rules are quite strict. Much more strict than the rules Congress itself is required to follow. We’ll see if this latest effort by the Fed proves successful in getting their stock trading out of the current news cycle.