Unemployment, productivity, and labor costs

Unemployment, productivity, and labor costs

meanwhile Goldman Sachs laughs in the face of an oil selloff.

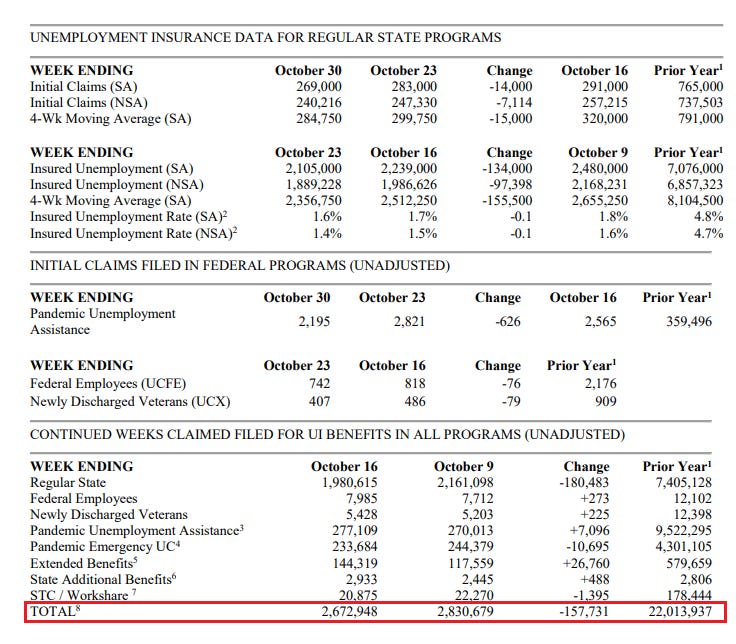

It’s Thursday, which means the Department of Labor posted the unemployment numbers.

Those on the unemployment dole are continuing to dwindle. In every practical sense, we are looking at full employment. Here’s a look at the 53 years of initial claims prior to March 2020. I’ve put in a red line where we are at today.

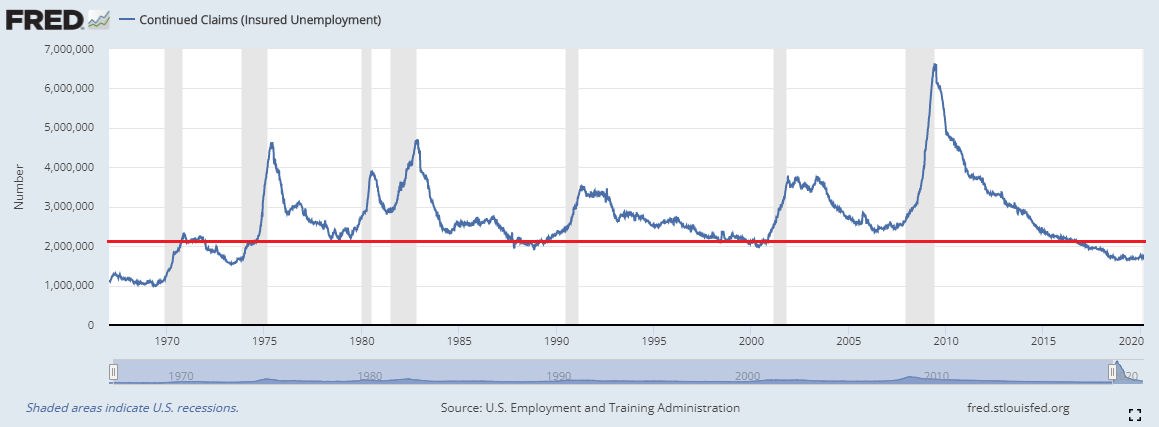

Here’s the same exercise with continued claims.

Anyone saying that the Fed is tapering on schedule or ahead of schedule is either delusional or a liar. The Fed is seriously behind schedule. Reviewing the Fed’s position, I’m reminded that the press conference that followed could have been the second to last press event for Fed Chair Jerome Powell. His tenure ends in February. I have serious doubts he’ll be retained by the current administration. US Treasury Secretary and former Fed Chair Janet Yellen laid it out in an article published by USNews. She has declined to say if she supported the reappointment of Powell and stated plainly that Biden should pick someone seen as a credible and capable policymaker.

"I think Powell has acquired that reputation, but there are other candidates too, who I think would be similarly perceived"

This is no ringing endorsement for the current track record at the Fed.

The left saw that Trump got whatever he wanted from Powell. Now that they are in power, they want the same easy money gravy train but Powell is now in taper-mode.

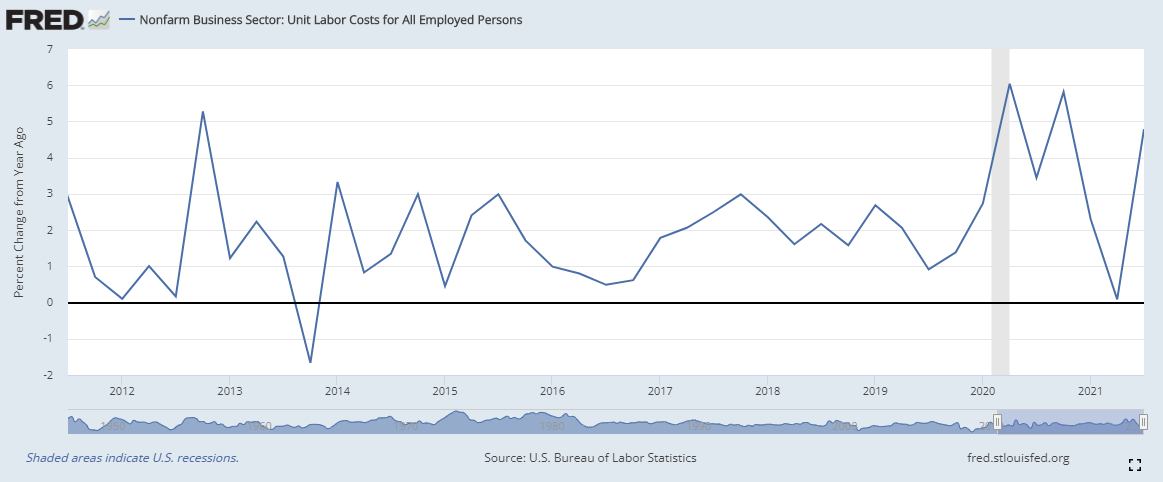

Even though the employment picture is resolving, employers are facing huge losses in productivity and rising costs of employment.

Above is the year-over-year comparison of unit labor costs for employers. Today’s number jumped to an annualized figure of 8.3%. This beat the market forecasts of 7%. It reflects a 2.9% increase in hourly compensation and a 5% drop in productivity. This could really eat away at those employers with tight margins. Another factor that is eating margins is the cost to get product to the store shelves.

")

Oil has been sliding lower since the 1st. WTI was as high as 84.75/bbl and has since dropped to 79.33/bbl. Goldman Sachs is unfazed. Their commodity analyst, Damien Courvalin, wrote that the bank’s bullish view remains unchanged. Goldman is betting heavily on oil getting to $90/bbl by year-end. The bank lays out the following reasons:

First, the oil deficit remains unresolved and requires higher oil prices.

Second, the current strength in oil demand remains a near-term tailwind as it is coming above consensus expectations (with OPEC’s demand assessment especially low in our view).

Third, the increasingly structural nature of the deficits will shift next year the bullish impulse to supply, requiring much higher long-dated prices. As for a larger increase in OPEC+ production at its next meeting on December 2, it may well be warranted with the strength in demand, bringing the global deficit to 2.5 mb/d last month, 0.8 mb/d larger than the bank had expected.

Now some of this is banker/analyst talk. It’s almost like a sub-language. Words like “tailwind”, “consensus expectations”, “structual deficits” all put me to sleep almost immediately. What I pull out of this banker/analyst talk is this;

the world is still using more oil than it is pulling out of the ground

near term future oil use is going to be higher than expected

OPEC is being relied upon to solve the issues with higher prices, even though OPEC has been slow to add more production and enjoys higher prices.

I find it troubling to be in agreement with Goldman Sachs but I believe they have the correct view on the subject. Oil prices are going to remain stubbornly high unless OPEC announces a large increase in output or the US faces a recession. Oil could very well be climbing it’s own wall of worry.

- Wikipedia")

So Powell is too slow to taper and the Dems think he is too fast and want him to be replaced...

And gold is still under $2,000?!!!

Man oh man 2022 is gonna be nuts.