Wait, what did he just say?

Media appears clueless at Jay Powell's statement and speech

The FOMC wrapped their two day meeting and Fed Chairman Jerome Powell released a statement and held a press conference discussing the Fed’s future moves. Chair Powell has gotten much better at talking a lot without saying anything of substance. At his first few meetings, he was nervous and often said too much causing confusion and turmoil in the market. He has now become a much smoother operator. Today’s press conference was much ado about nothing. Jay’s statement was very dovish and the market reacted by maintaining it’s big morning push. However, once the Q&A started, the press went crazy. This caused traders to second guess their morning buys and the indices reversed course.

It was a big shock to me that the press pushed so hard on the Fed chair for more details when it was obvious from his statement that there would be none. Again and again the press was looking for something concrete but Powell stood his ground and kept to the script, (para-phasing) ‘we will continue to manage monetary policy by monitoring the data’. They really hammered hard with questions wondering if the Fed could control inflation without letting the general economy fall into a recession.

The playbook was laid out very plainly. Here’s what the Fed stated in four major points.

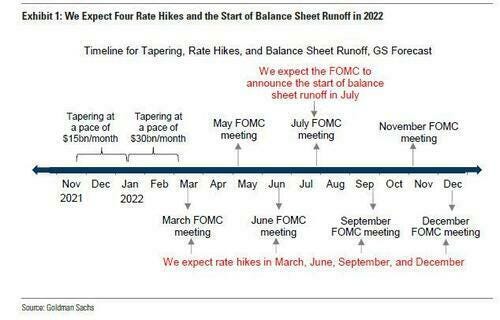

The Fed will end it’s asset purchases in March

The Fed believes it will soon be appropriate to raise interest rates

The Fed’s balance sheet will start after raising interest rates

The Fed intends to primarily hold Treasuries and are moving away from mortgage-backed securities

This was very plainly stated but no real dates were given. It is obvious that the Fed wants to take this slow. The Fed is going to look at their signals (inflation, employment, and the stock market) before they make a rash decision.

This was a serious tight-rope walking act that Jerome performed. The press did him no favors in the Q&A. He certainly played up the Covid narrative to his advantage. Now traders are left to piece it all together.

Danielle DiMartino Booth, former adviser to the former president of the Dallas Fed, said it this way:

“The Fed’s biggest challenge is figuring out how to implement policy measures that are hawkish enough to lower inflation, but that also keep financial markets afloat, because volatility in financial markets may bleed into an economy that is already showing signs of slowing. The Fed is faced with choosing the lesser of two evils."

My belief stands firm. The Fed is removing the punch bowl of liquidity to the market. This is going to cause increased volatility. Once the Fed begins raising interest rates, the market could react favorably at first, but it will then struggle. This will be especially true of any high or negative P/E growth stocks. Investors will not be able to tolerate promises of growth as those future cash flows get discounted to the present at a reduced rate. Once the Fed allows its balance sheet to slowly reduce in size through runoff, this will exacerbate the market’s liquidity issues and most likely cause something to break. Once that happens, the Fed will be in a tight spot. Do they cut rates to zero and go on a balance sheet expansion bonanza allowing inflation to run hot or do they keep to the plan in an attempt to prevent inflation from becoming “entrenched”? My money is on the former. Why would I believe this?

I dunno, just a hunch I guess.

Here’s the Fed’s estimated blueprint from Goldman Sachs.