Why I love gold right now

and a preview of the busy week ahead

I have an affinity for the yellow metal. It’s true. I won’t deny it. There is something about gold, when it is in your hands, you can just tell it has real value. Unfortunately I have been a terrible trader when it comes to gold. I get emotionally involved which is a big no-no on Wall Street. I’ve bought on the way up, held for longer than I should have and gotten burned. I get caught up in the idea that “this time could be the big one”. This would be when gold takes off and we hit that inflationary spiral. I’m sure this is due to reading into the economic environment and only seeing inflation coming. Some in the Austrian community have been pounding the table about inflation since 2008. That’s over a decade! Pounding that long would make my fists hurt. I’d have to re-examine the basis for my investing thesis.

So here is my investing thesis for gold. I’m going to lay it out as simple as I can and where I think we are going to see gold go to. But first, we must understand why investors shun the yellow metal. Many of the big name investors avoid investing in gold for one big reason. It has no earnings, it pays no dividend. Warren Buffett put it best, gold has “no utility”. Jason Snipe of Odysssey Capital Advisors says it this way;

"It doesn't produce anything and that's why from a long-term perspective, it's a hard asset to invest in." It's prudent portfolio management to have maybe a small allocation there but this is not an asset that you want to be heavily entrenched into if you're looking for long-term yield."

For these big guys, gold is an unproductive asset. This means that the gold you hold won’t produce more gold. When you compare this to a company like Exxon who produces oil and pays a dividend, it is easy to see why these big investors would prefer a productive asset.

Unfortunately, this is the wrong way to look at gold. This is because gold is money.

If you are familiar with FX trading (that is trading currencies), this comparison looks much more appropriate. The difficulty with using this approach is that gold is not the currency of any one country. When you trade FX, you are comparing a country’s economic drivers and central bank actions. You want to analyze that country as a whole to gauge it’s economic stability and future. With gold this is not possible. Gold should be considered more of a mathematical constant. That means it is a key number whose value is fixed (i.e. pi or e). This means gold doesn’t fluctuate, the currencies around it do.

If you did your homework over the weekend, you would have seen this chart:

Gold did well from 1972-1974 and again from 1976-1980. These two periods were plagued with stagflation. Inflation was running high while the economy stagnated. It led to more dollars in circulation and businesses reporting poor earnings.

Gold performed as expected during the other inflationary periods that Michael Lebowitz studied.

When you understand gold as a constant you see that gold didn’t achieve out-sized returns. It stayed constant during these periods as more dollars were being introduced into the money supply. This played about similarly with the other top returners oil and coal. Also, the companies whose earnings outpaced inflation were able to do ok. Those that couldn’t struggled and failed.

On Friday, Bloomberg put out a piece on the potential for a run on gold as investors begin to worry about inflation. They interviewed two big names in the gold mining sphere. David Garofalo and Rob McEwen both believe that investors will begin piling into gold soon. They believe prices could quickly hit $3k. McEwen has even predicted $5k gold prices. McEwen believes this will happen in short order.

“I’m talking about months. The reaction tends to be immediate and violent when it does happen. That’s why I’m quite confident that gold will achieve $3,000 an ounce in months not years.”

We have people on the inside who are sounding the alarm. They see shortages of labor and rising costs. They’ve also seen what the other metals have been doing.

We have seen an enormous amount of dollars added to circulation in the last two years. The money supply is still running above trend. The Fed will publish the latest figures on Tuesday. This will be something to watch closely. However, if gold is a constant, this recently added money should goose the price of gold like it has goosed the price of the other metals. Even Jack Dorsey sees inflation coming.

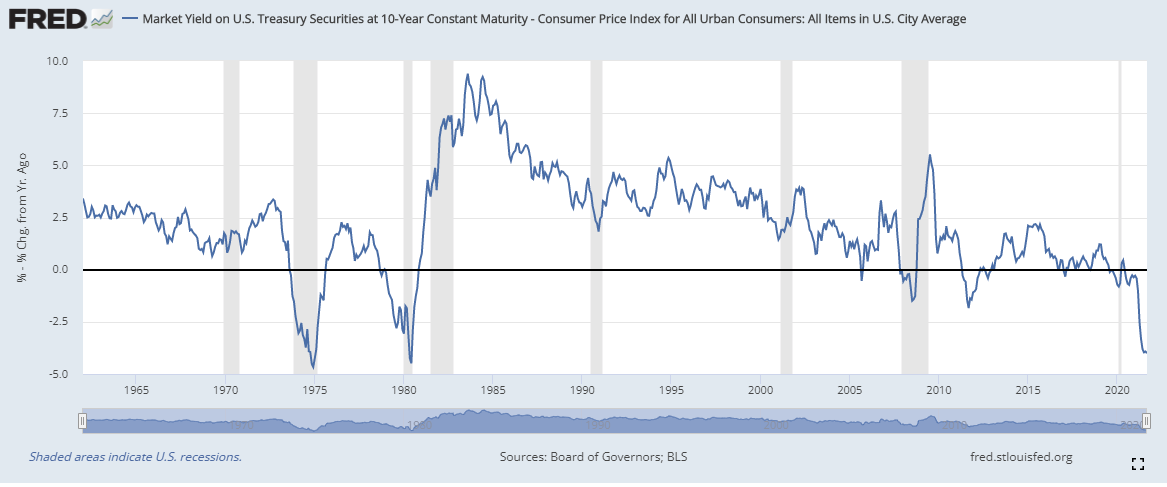

One of the last underpinnings to my thesis relates to bonds. Bonds are an important investment vehicle for the big players on Wall Street. Bonds have been in a bull market for over 40 years. This has driven yields to extreme lows. This is the 10-year treasury. According to this chart, if you were to buy the 10 year treasury, you’ll get paid 1.68%.

However, if inflation runs above 1.68% for the ten years you hold the bond, you would actual lose buying power. Here’s a look at the 10-year minus the CPI.

We are now in dangerous company with the 10-year yielding a negative return when you take inflation into account. The prior two periods where the 10-year minus the CPI ran this low was 1974-1975 and 1980. Looking back at Michael Lebowitz’s graph, we know what does best in this environment, gold. This is because the investors that are holding bonds think they are safe. When inflation eats away at your yield, you have to change gears. You have to find something safer than bonds. You have to find a constant in this money printing madness. That constant is gold.

Some may argue that bitcoin has replaced gold as a constant. I would agree that, like gold, bitcoin is an unproductive asset and that it could be a substitute for gold. In fact, I think gold has lost some of it’s luster to bitcoin. However, gold has proven itself with over 4,000 years of data. It has been money for a lot longer than bitcoin. I would not look down on anyone using bitcoin as an inflation hedge, like one would use gold. I think they could be interchangeable. With the advent of bitcoin ETFs (BITO), it is now getting easier than ever to hold bitcoins. Ultimately I don’t know enough about bitcoin to give it a ringing endorsement. I do know enough about gold and I think we are about to see it take off.

In review, I’ve gone over how investors should view gold (like a currency constant), what the insiders are saying ($3k gold in short order), and why now is the time (bond yields are deeply negative). Finally, I’ll wrap up with a prediction. Like the industry insiders, I can see how $3k gold is easily achievable. When you look at Michael Lebowitz’s graph, you see that oil and gold ran neck-and-neck cumulatively through the 7 inflationary periods. Oil has achieved 72% gains year-to-date. If gold were to have 72% gains this year, it would be at $3,096 an ounce. I expect this could be easily achievable for gold but beware, I’ve been burned before. Some pitfalls to watch out for would be Fed announcements. Investors look to the Fed because they believe the Fed is in control. Every hawkish announcement that they make will suppress the gold price. Every time they talk about tapering asset purchases or raising interest rates a little bit of the wind will go out of gold’s sails. This means we should have an excellent setup to purchase gold next week when the beginning of the taper is set to begin.

This is a big week for Wall Street. We will see the following economic data releases:

Tuesday October 26 2021

S&P/Case-Shiller Home Price Index (my favorite inflation gauge!)

H.6 Money Supply

Wednesday October 27 2021

Durable Goods Orders

EIA Crude, Gas, Fuel, and Heating Oil Reports

Thursday October 28 2021

Initial Jobless Claims and Continuing Jobless Claims

Friday October 29 2021

Personal Consumption Expenditures (PCE) and Core PCE Indexes

University of Michigan Consumer Reports

Baker Hughes Oil Rig Counts

This week is also a big week for companies to report earnings.

I’m watching closely the reports for Visa (are consumers spending more?), Teck (natural resource miner), and the oil companies; Exxon, Chevron, and Philips.

In addition to these, Cameco (CCJ) and Energy Fuels (UUUU) will have earnings releases on Friday. This will provide great insight into whether these companies are stockpiling uranium or securing contracts for sale.