The Meltdown Resumes

The Meltdown Resumes

and how regime uncertainty adds to the mess

The market got hit with a double whammy before the open. The first bad news to hit was the CPI.

The CPI has resumed it rise higher. This spooked the market because the herd thought that the Fed had it under control and that a slow increase in the Fed Funds Rate was going to tame the inflation beast. The last time we had inflation increasing at 8.5% year-over-year, the Fed Funds Effective Rate was 12.37%. This was December 1981. Today it sits at 0.77%.

Admittedly this print caught me off guard. I had expected the CPI to cool slightly before it resumed its rise higher. BoA has the heatmap to see what components caught fire.

The big components that jump out at me are food (1.17%), energy (3.9%), shelter (.61%), and airfare (12.56% month-over-month!). Since food and energy get stripped out of the “core” inflation data, it came in at 6.0%. This was down slightly (-0.12%) from April’s data.

Shelter is such a large component of the CPI (32.4%), that a .61% increase month-over-month can really move the needle. This is also the hottest the shelter factor has risen in the past year. Looking at the year-over-year heatmap, shelter has a long ways to go to catch up to housing prices which have risen over 20% year-over-year.

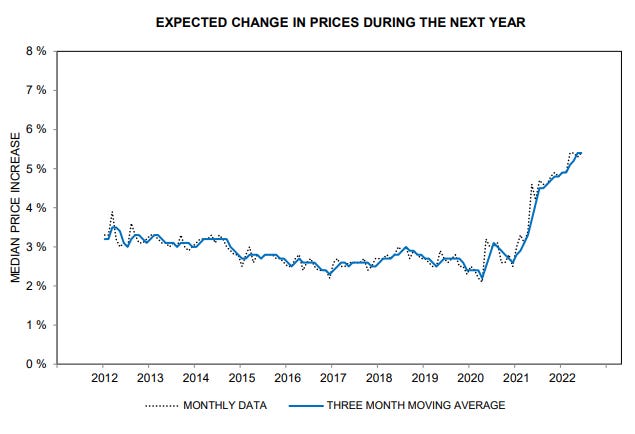

The other news that the market had a hard time digesting was data from the University of Michigan. UofM conducts consumer sentiment and inflation expectation surveys on a monthly basis. This morning saw the preliminary release of June’s data and it did not look good.

These charts are ugly. Consumer sentiment has fallen off a cliff. Expectations are at a low not seen since 1980 while inflation expectations have moved higher to 5.4%.

The inflation we are experiencing is a supply-side shock. Therefore, the US needs supply-side reform. We need a revitalization of our domestic economy. Industry and production needs to be welcomed back. To tackle this, many reforms need to take place. In addition, regime uncertainty needs to end. Don Boudreaux tackled this in a recent letter to the Wall Street Journal.

Here’s a letter to the Wall Street Journal:

Editor:

Wayne Stoltenberg and Merrill Matthews make a compelling case that oil exploration, drilling, and refining will remain depressed for as long as government keeps threatening to suffocate that industry with regulation and taxes. (“Why Energy Companies Won’t Produce,” June 9). This depressed investment reflects an instance of what economic historian Robert Higgs calls “regime uncertainty,” which he describes as “a pervasive uncertainty among investors about the security of their property rights in their capital and its prospective returns.”*

Ominously, regime uncertainty’s lethality to economic growth need not be confined to a single industry. Higgs documents that such uncertainty was the root cause of the Great Depression’s length:** As FDR’s administration became increasingly hostile, in both word and deed, to free markets, the entrepreneurs and investors who drive economic growth became dormant economy-wide as they feared that they’d be robbed of the fruits of their efforts and investments.

If Progressives persist in their infatuation with socialism, while many prominent conservatives demand industrial policy and draconian regulation of Big Tech, regime uncertainty will surely expand beyond the energy industry to asphyxiate much, and perhaps all, of the economy.

Sincerely,

Donald J. Boudreaux

Professor of Economics

and

Martha and Nelson Getchell Chair for the Study of Free Market Capitalism at the Mercatus Center

George Mason University

Fairfax, VA 22030

* Robert Higgs, Depression, War, and Cold War (New York: Oxford University Press, 2006), page 5.** Robert Higgs, “Why the Great Depression Lasted So Long and Why Prosperity Resumed after the War,” Independent Review, Spring 1997, pages 561-590.

There are two sides to this inflation coin, monetary policy driven by the Fed and fiscal policy driven by Congress/White House. While the Fed certainly needs to act more responsibly, the White House and Congress also need to end their toxic rhetoric towards anyone making a profit (oil and gas, food producers, and now shipping companies). All these actions drive investment away from where it is needed most.

Now its time for Jerome Powell to get back to work. I imagine we’ll see increased posturing around 75 basis point hikes.

The Fed is really going to feel the heat now. The bond selloff program is just beginning and they are already going to feel pressure to scrap it. Yet, they can't turn this ship around with the CPI sitting at an insane 8.6%. Folks really need to grasp how insane that number is. With all the chicanery around how the CPI is calculated, they still found a way to match CPI numbers we haven't seen in 40 years. I don't think they can take their foot off the brakes. The inflation numbers are too politically devastating to swallow. Even if they stop the bond selloff program, they can't juice the money supply without risking 15-20% CPI and massive political unrest. My guess is that every Fed insider is using this opportunity to get everything they have out of the stock market. The crash is coming and there is nothing they can do about it.