The pressure is intensifying

Don't get squeezed out

Recent market action points directly towards a short squeeze. Retail traders are piling in and institutional traders are making their way to the exits. Hedge funds are coming under increasing pressure from redemptions and are already shuttering their businesses. The end of June will be an important time for these market goliaths. Any redemptions requested in the previous quarter will need to be funded by the end of the month. That means more selling pressure could be coming.

The hedge funds that are going to experience the most pain are those that were riding high on the tech wave. I’m specifically talking about anyone who replicated or attempted to replicate Tiger Global Management. I should preface this with saying that those at Tiger did an amazing job over their run. This hedge fund was founded during the tech selloff in 2001. Between 2007-2017 they raised the highest amount of capital among venture capital firms. However, this year they failed to see that the peak was in and have lost over 52%. This is devastating for a firm that boasts an AUM figure of $124,655,466,641 and holds $26,641,819,000 in stocks. These stocks that they hold will see selling pressure as investors pull their money out.

This has slowly led me to review my own investment choices. When you see a mega-fund like Tiger get crushed, it is extremely humbling for someone whose holdings are less than 0.00001% of theirs. It shows that the market doesn’t play favorites.

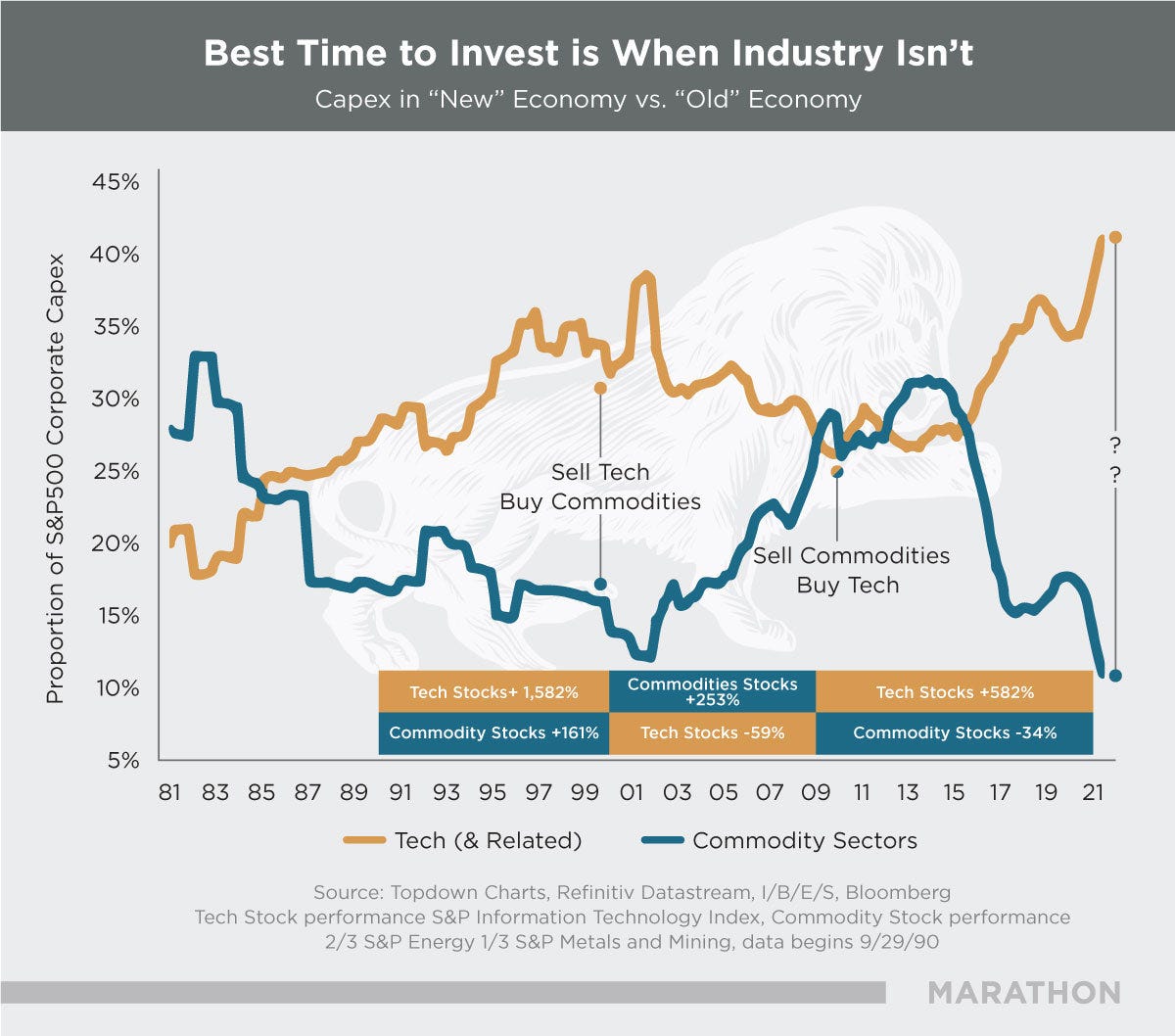

I am a firm believer that a great rotation is happening. It started at the end of last year and it could very well carry on for a decade. What I’m talking about is a commodity super-cycle.

There have been three major commodity cycles (1930-1940, 1970-1980, 2000-2010). I found an amazing resource that goes into great depth on these cycles. It’s a letter put together by Goehring & Rozencwajg. They believe this commodity bull cycle is in its infancy and those that hold on for the ride will be well compensated on the other side. I’m going to be heavily quoting this material because I think it is where the market is going.

They reviewed the stock market versus a basket of holdings. Those holdings were divided into four groups.

“Constructing a natural resources equity portfolio that consisted of 25% energy, 25% metals and mining, 25% precious metals, and 25% agriculture would have significantly beaten the stock market in each of these cycles.”

Their view of the 1930-1940 commodity market:

“For example, had you invested in such a natural resource portfolio in 1929, your return would have been 122% by 1940, which doesn’t sound like much, but compared to the Depression ravaged stock market, the returns were almost spectacularly good. Between 1929 and 1940, the stock market fell 50%. Also, the 1930’s was a period of chronic deflation and consumer prices fell over 20% between 1930 and 1940. In real terms, commodity prices (and related equities) offered real returns of almost 180% -- not bad in a period that included one of the greatest bear markets in history and a full-blown banking crisis that required the temporary suspension of the world financial system.”

1970-1980:

“In 1970, a similarly constructed natural resource equities portfolio would have returned 400% by 1980, a return that handily beat the stock market which returned only 80% for the decade. Inflation was a huge problem in the 1970s and consumer prices advanced almost 130% for those 10 years. Natural resources not only provided excellent relative returns versus the stock market, but they provided investors with nominal returns far above the inflation rate as well.”

And finally, 2000-2010:

“And finally in 2000, a similarly constructed natural resources equity portfolio would have returned 360% between 1999 and 2010, significantly outperforming both the stock market, which returned nothing during that time period, and the inflation rate, which advanced 35% over those 10 years.”

I believe we are firmly in the grips of another one of these runs in commodities. I also believe that Robert Wenzel was leading to this point and why he stressed the SOG portfolio. Commodities have been starved of capital for far too long. This piggy-backs on a comment thread from June 8th. The market always deals in cycles. This is the ultimate theme of the stock market. Quoting myself about shipping companies:

“After years of neglect and the absence of investment, many companies went under. They stopped the development and purchasing of new boats. After a few years of consolidation, shipping rates slowly began to rise.”

We have witnessed this kind of business destruction in more than just shipping companies. When this kind of business destruction and then consolidation happens, it is only a matter of time before these businesses come roaring back. This all leads me to a very interesting path. I’m beginning to change my philosophy of utilizing stop-losses and instead, own a diverse array of holdings that will work with the commodity super-cycle theme. I even have a name for it. The diamond hands portfolio. This is because I won’t be selling any of these holdings until these companies either reach a ridiculous return or go bankrupt. I’ll be working out the details of this portfolio through the next two weeks which means my blog postings are going to be less. I’m going to leave the last words of today’s post for Goehring & Rozencwajg:

“The biggest risk for investors is selling too soon.”

I notice that commodities remained undervalued from roughly the mid 1950s to the mid 1970s. I wonder if there's a more precise way to know when the commodity time is right.

Great information today. I am curious, would you be willing share some recommendations of holdings - similar to Robert Wenzel's EPJ Daily Alert?